Donating To Charity Using Life Insurance Makes Financial Sense

During the course of my 26 year career, I’ve helped several Canadian charities set up direct mail marketing campaigns promoting charitable gifting using life insurance. The results have been positive with millions of future dollars being donated to charities, while simultaneously creating a lasting legacy for the donor. I’ve also noticed, Canadian charities becoming increasingly proactive in their marketing strategies to find long-term, tax effective funding alternatives. Giving through life insurance will provide that alternative funding charities are looking for while providing their donors with some unique advantages.

During the course of my 26 year career, I’ve helped several Canadian charities set up direct mail marketing campaigns promoting charitable gifting using life insurance. The results have been positive with millions of future dollars being donated to charities, while simultaneously creating a lasting legacy for the donor. I’ve also noticed, Canadian charities becoming increasingly proactive in their marketing strategies to find long-term, tax effective funding alternatives. Giving through life insurance will provide that alternative funding charities are looking for while providing their donors with some unique advantages.

- Advantages to the donor include:

- A substantial monetary gift and legacy for less cost.

- Insurance premiums paid can qualify as a tax credit.

- Unlike a will, insurance policies are not public information and provide confidentiality.

- On death, insurance proceeds are passed directly to the beneficiary and can avoid probate fees.

- A charitable gift insurance policy is protected from the claims of the donor’s creditors.

Donors who purchase a charitable gift life insurance policy are entitled to federal and provincial tax credits. The federal charitable tax credit rate is 15% for the first $200, 29% of the balance (33% for donors in the top marginal tax bracket). The provincial charitable tax rates for Ontario are 5.05% on the first $200, then 11.16% on the excess of $200 claimed that year (in addition to the 11.6%, there is also an Ontario surtax savings which is reduced as a result of the credits). This is a non-refundable tax credit and can only be used to reduce taxes owed. The value of these tax credits make charitable giving an attractive tax savings vehicle for many Canadians.

To get a quick estimate on a charitable tax credit for the year, I like using the Charitable Donation Tax Credit Calculator http://www.cra-arc.gc.ca/chrts-gvng/dnrs/svngs/clmng1b2-eng.html. It quickly calculates your federal and provincial total tax credits based on your personal taxable income in the province you reside. It also calculates the first-time donors’ super credit, an extra federal tax credit for money donated by first-time donors up to $1,000.

How To Set Up The Insurance Policy

Let’s look at the two most common ways a life insurance policy is set up with a charitable donation in mind. Scenario #1 assumes the charity owns the life insurance policy and the donor makes the premium payments on behalf of the charity. Scenario #2 assumes the donor owns the policy and the insurance proceeds are gifted to the charity when the donor dies.

Scenario #1 - Charity-owned Insurance Policy

This is what I call a three-party life insurance contract and involves the charity, the donor, and the life insurance company. The charity is the owner and the beneficiary of the insurance policy. The donor is the life insured and pays for the insurance premiums on the charity’s behalf. The charity then issues a tax receipt to the donor every year. A charitable tax credit is available to the donor for the premium payments. The donor can then claim amounts of up to 75% of their net income.

With this type of set up, I usually recommend a permanent insurance plan that accumulates cash values. This is useful to ensure the charity receives a monetary gift in case the donor can’t make future premiums. The charity would then have the option to cash out the policy as the charitable donation. Alternatively, if the charity wishes to keep the plan going, they have the option to pay future premiums or stop paying and reduce the death benefits using a provision called reduced paid-up insurance.

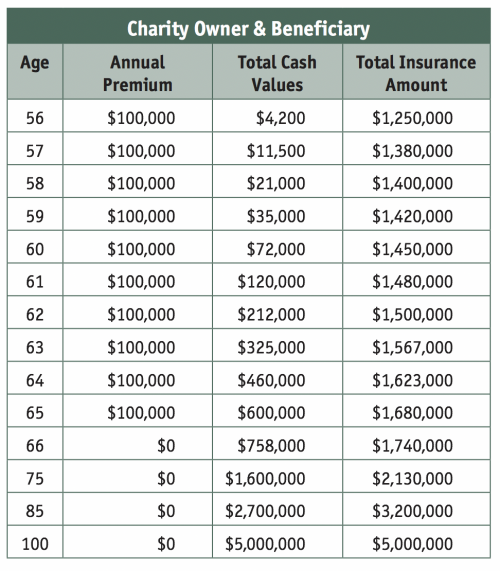

Charitable Gift Insurance Policy Illustration

The table below illustrates a 55 year old male purchasing a whole life participating insurance plan with an annual premium of $100,000. The charity will be the owner and beneficiary of the policy and the premium payments are made by the donor (the insured) for a maximum of 10 years. On the death of the donor, the charity receives the total death benefit amount as the charitable donation. If the donor cannot continue premium payments (using age 62 as an example), the charity then has the option to cash out the plan and receive a cash donation of $212,000.

(Illustration provided by a highly rated Canadian insurer for a 55 year old male non-smoker issued at standard rates. Total cash values and total insurance amounts include a guaranteed portion plus a non-guaranteed dividend portion. The current dividend scale shows a 5% dividend return. Increases in policy cash values and policy death benefits will vary depending on the companyís future dividend earnings).

For the donor, the annual premium payments qualify for a donation tax credit. For income taxed at the top marginal tax rate of $220,000, donation tax credits are available at 50.41%. For income taxed at any bracket below the top marginal tax rate (i.e. income below $220,000) the donation tax credits are available at 46.41%. Assuming the donor has an annual income of $225,000 in Ontario, his income will be taxed at a marginal rate of 53.53% and his average tax rate would work out to be about 37.03%, resulting in close to $83,318 in tax payable.

Using an online calculation tool (ww.taxtips.ca/calculators/canadian-tax/canadian-tax-calculator.htm) the $100,000 donation would result in approximately a $45,000 donation tax credit. The donation credits of $45,000 reduce the tax payable dollar for dollar. The full tax credit can be applied to tax payable. The end result would mean a tax bill close to $38,318 ($83,318-$45,000) instead of $83,318. Based on these numbers, the donor doesn’t need to be concerned about the 75% net income limitation. He would be able to claim up to $168,000 ($225,000 x 75%), so his $100,000 donation could be fully used.

Scenario #2 - Donor-owned Insurance Policy

With this scenario the donor will own the insurance policy and the charity will be the beneficiary. This allows the donor to have full control over the insurance policy. It also gives the donor more flexibility in case the donor changes their mind on which (if any) charity receives the gift. The charity risks receiving no gift at all since ownership of the policy gives the donor the option to change the beneficiary at any time.

Since the donor owns the insurance policy, the donor won’t qualify for a charitable donation tax credit for premiums paid. However, when the donor dies, the insurance policy’s death benefit can be paid to the charity. A charitable donation tax credit will arise on death, and the death benefit from the insurance policy can be used on the donor’s final income tax return. Since the gift is made directly to the charity on death, it will not pass through the estate of the donor and will not be subject to probate fees or estate creditors. Once the charity receives a gift of the life insurance policy proceeds, they will then issue a donation receipt to the donor. The donor can then claim charitable tax credits for amounts of up to 100% of income on their final tax return. With this type of set up, I recommend a permanent, limited-pay type of insurance plan. However, cash values may not be so important, when compared to a large death benefit. A universal life or a whole life non-participating insurance policy can work well for this scenario. For example, using a universal life plan for the same male age 55 in the previous example, it’s possible to pay a one-time lump sum of $1million (or a series of 5 payments of $200,000) and gift a death benefit charitable donation of over $3 million.

Planned giving using life insurance is an effective estate planning strategy for people who want to support a charitable organization and substantially increase their annual bequest while reducing their tax obligations. For charitable organizations gifting through life insurance helps long term funding. A direct marketing campaign to current and future donors would be useful to both parties since many donors are not aware about the option to donate large sums of cash through life insurance.

Rino Racanelli is an independent insurance advisor in Toronto, ON. Email: racanelli@sympatico.ca, www.CorporateLifeInsurance.ca