The Christmas Gift That Keeps On Giving

With the Christmas season soon approaching, parents and grandparents will once again be scrambling for that perfect gift to give their children or grandchildren. With a countless number of choices out there, many will take the easy route and give cash. I always liked getting cash. The only problem was I spent it right away instead of setting some aside for future needs.

With the Christmas season soon approaching, parents and grandparents will once again be scrambling for that perfect gift to give their children or grandchildren. With a countless number of choices out there, many will take the easy route and give cash. I always liked getting cash. The only problem was I spent it right away instead of setting some aside for future needs.

Setting aside money for your children and grandchildren’s future is smart planning. With so many options available, it can be difficult to choose which type of savings plan will meet their future needs. I believe several key requirements in a child’s savings plan should include safety, guarantees, tax-advantaged cash growth, and control by the person who is making the deposits.

A popular but less talked about savings plan that has all of the above requirements and more—participating children’s life insurance. Participating insurance plans for children have been offered to Canadians since the late 1800s, and have remained a stable financial product throughout its history.

A participating policy is a combination of permanent life insurance protection along with a tax-advantaged guaranteed cash value growth and the opportunity to earn dividends. Participating simply means the insurance company pays annual dividends to the policyholders, which are generated from the profits of the company.

If your parents or grandparents purchased one of these plans for you when you were a child, then you will understand and appreciate the value of this product. You may have used the cash values built up in your insurance plan to help pay for a post-secondary education or help fund other life events like a wedding, graduation vacation, or even a down payment on your car or home.

For those who never had a plan, Christmas time can be the perfect time of the year to consider how you can help your children or grandchildren get a head start on life.

A permanent insurance plan for a child offers a number of benefits:

- Affordability—the younger your child, the lower the cost will be.

- No income tax is payable on the growth of the cash values while it remains in the policy.

- Potential dividend earnings.

- Guaranteed payment plans 10 or 20 years.

- Protection for life-changes pertaining to health, jobs, or hobbies could make a child uninsurable when they get older. Having insurance early can protect their future insurability.

- Transfer of the ownership of the policy between the parent or grandparent and the insured child without tax implications. Known as a non-arm’s length transfer in section 148 (8) of The Income Tax Act, that allows for a tax-free rollover to a child.

- Depending on your child’s age, you can customize your policy and protect it by adding the owner waiver on death and disability benefit. These optional benefits can provide additional protection while ensuring your premium is paid if the unexpected happens.

My personal experience is a good example of how some of these benefits work. My father purchased a participating insurance plan for me at the tender age of 15 days (at that time 15 days was the earliest age at which you could purchase a plan). It was a simple, low-cost, dividend-paying, permanent plan that was guaranteed to be paid up in 20 years. Included in the plan was the waiver on death benefit for 20 years at minimal cost.

Sadly, my father passed away 10 years after the plan had started. The waiver of death rider would require the insurance company to pay the premiums on my policy for the next 10 years until the plan was fully paid up, which they did.

When I made the decision to go to university (my father’s wishes), the policy ownership was transferred over to me with no tax consequences. By signing the policy over, any future tax implications on cash withdrawals would be my responsibility. At age 21, I decided to cash out my policy (in hindsight I should have just cashed out the dividends and kept the plan in force, a mistake I have regretted to this day). At that time, there was enough money in the plan to pay for my first year of university (although I could have used the cash for anything I wanted). The following year the insurance company sent me a T3 capital gain income of $648.00 to be included in my personal tax return. This had little effect on my tax payable that year since I was a full-time student and only a part-time worker.

Participating Insurance And/Or Registered Education Savings Plans (Resps)

Registered Education Savings Plans (RESPs) have become a popular choice since the government program was first introduced in 1972. Particularly attractive is the 20% government grant available to contributors. Since most of us are familiar with the workings of RESPs, I won’t get into details. The important point about RESPs is they must be used for a post-secondary education.

Let’s look at some comparable numbers for these two popular children’s plans.

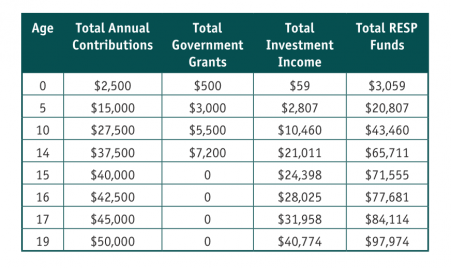

Below are a RESP illustration and a participating insurance illustration for a newborn child using an average rate of return of 5% for both products?

For the RESP illustration, I have applied some basic rules to RESP investing.

- A lifetime maximum contribution limit of $50,000 per child.

- Government to contribute a maximum lifetime grant of $7,200 per child.

To receive the annual maximum government grant of $500 per year, an investment of $2,500 per year per child is required.

The chart above shows a total contribution limit of $50,000 for the RESP. At age 14, the maximum government grant of $7,200 has been achieved. After 19 years of deposits, the investment amount has grown to $40,774 and a total fund growth of $97,974.

When the RESP funds are withdrawn, there is no tax implication for the $50,000 contribution portion. For the investment income and government grant portion, (Education Assistance Payment), a T4A will be issued to the child (beneficiary) regardless of who receives the withdrawal.

Let’s invest the same $2,500 every year for 20 years, for a total amount of $50,000, into a children’s participating insurance plan. At 20 years the chart below shows the total cash value has reached $60,000 and the insurance portion has grown to $437,000. After 20 years, the plan is paid up and continues to grow and receive dividends every year until the age of 100. The rate of growth with participating insurance is impressive even when the plan is paid off. Of course, the cash values can be used for any purpose besides a post-secondary education. When the cash value is withdrawn only the portion that is above the adjusted cost base of the plan (the capital gain) is taxable.

Chart assumptions: Juvenile male participating insurance plan using 5% dividend scale from a highly rated Canadian insurer. Actual results will vary based upon the actual dividend experience of the insurance policy. There are a variety of factors affecting the dividend performance of a permanent insurance plan; mortality expenses, lapses, and investment returns. Investment return is the most important factor which only affects the non-guaranteed values of a participating policy and not the guaranteed values. Depending on the insurance company, the premiums paid are invested in a diverse asset-mix. Investments can include: government and corporate bonds, fixed income, equities, real estate, GIC’s, and short-term commercial mortgages.

Summary

RESPs continue to be the popular choice to fund a child’s post-secondary education. However, there are limits and rules to RESP investing that must be taken into consideration. You should ask yourself if the RESP will provide enough cash to fund your child’s entire education costs and if the lack of flexibility in choosing where to use the RESP funds will be a drawback.

Participating life insurance can also make sense because it provides your child with lifelong benefits. In addition to providing security and protection through the life insurance component, it provides an additional source of funds for education or any other life event.

Whether purchased on its own or to complement an existing RESP, participating insurance provides that extra tax-sheltered cash needed along with the flexibility in determining when the money will be used. Whatever the life event, it’s good to know you have the flexibility to determine when to withdraw the cash and give your child or grandchild a helping hand.

Rino Racanelli is an independent insurance advisor in Toronto, Ontario. Email racanelli@sympatico.ca. Visit www.corporatetaxshelter.ca.