Corporate-owned Permanent Insurance: Good Tax Shelter For Business Owners Despite New Law

On December 16, 2014, Bill C-43 “Economic Action Plan 2014 Act, No. 2” received Royal Assent, with provisions coming into effect on January 1, 2017. The legislation introduced changes that reduce tax-sheltering options to business owners looking to add a corporate-owned, tax-exempt, permanent insurance product to their portfolio. Despite the changes, can corporate-owned insurance remain a good tax shelter for business owners and will this unique product continue to play a valuable role in estate planning?

On December 16, 2014, Bill C-43 “Economic Action Plan 2014 Act, No. 2” received Royal Assent, with provisions coming into effect on January 1, 2017. The legislation introduced changes that reduce tax-sheltering options to business owners looking to add a corporate-owned, tax-exempt, permanent insurance product to their portfolio. Despite the changes, can corporate-owned insurance remain a good tax shelter for business owners and will this unique product continue to play a valuable role in estate planning?

If you’re a successful business owner or a key shareholder of a Canadian controlled private corporation, you may have set up a holding company to invest your business profits. Since Canada Revenue Agency considers assets held in your holding company to be passive income, they are taxed at the highest corporate tax rate. In my home province, Ontario, the combined federal-provincial tax rates are as follows:

Interest income, rent, royalties, dividends from a foreign corporation, and other income 50.17%.

Capital gains 25.09%

Dividends from Canadian corporation 38.33% (refundable tax).

The high tax and the decrease in wealth due to loss of compounding growth can make these types of investment less desirable.

A solution would be to invest a portion of the profits into a corporate-owned, tax-exempt permanent insurance policy. A tax-exempt insurance policy is defined in The Income Tax Regulations 306 and 307 and will immediately increase the estate value of a company’s shares. There is a mechanism that allows the death benefit proceeds to go tax-free to shareholders through the corporation’s Capital Dividend Account (CDA). The CDA is a notional account that keeps track of the tax-free amounts accumulated by a private corporation, which can be distributed to the corporation’s shareholders. The CDA credit is unique to corporate-owned life insurance. The Regulations also provides that the cash value accumulation in an insurance plan is exempt from annual accrual taxation, provided certain conditions within the regulations are met.

Let’s compare two low-risk corporate investment strategies using a case study.

Case Study

Tax-exempt permanent insurance plan vs. Traditional guaranteed investments

Bob is a successful business owner earning $425,000 annually. He is 45, married, and has two dependent children. The investment portfolio in his holding company’s account has a current value of $3.8 million. Every year his company pays significant tax on the income generated from these passive investments. He is looking for an effective strategy to transfer some of these passive corporate assets from a taxable environment to a tax-advantaged environment and ultimately reduce his capital gains tax on corporate shares at death.

Presently, 60% is invested in Canadian, U.S, and International equities with the remaining 40% invested in capital property. Bob is concerned about the lack of diversification in his corporate portfolio because he has only two asset classes and no fixed low-risk products. Since he is now in the middle of his career, he feels he should be reducing his risk and his corporate tax bill.

Bob is looking for guarantees and to maximize the value of his corporation on death when it would eventually pass on to his two children. He also wants to minimize the amount of corporate tax he is paying. Bob decides to move approximately $100,000 per year for the next 10 years from his 3.8 million corporate account into a fixed lower-risk investment.

Bob was presented with two scenarios for low-risk investing into his corporation:

invest the amount into a guaranteed interest-paying portfolio (GIC type fund) that protects his principal investment and returns interest.

invest the amount into a corporate-owned tax-exempt permanent insurance plan.

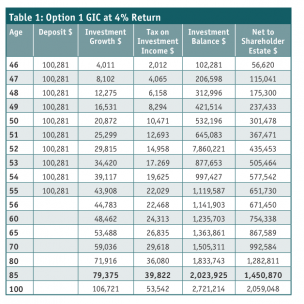

We can compare the two investment options using an annual investment for both that worked out to be $100,281. Since tax laws and rates of returns are subject to change, we can use reasonable assumptions for future earnings and growth.

For the tax-exempt insurance plan, we will use the insurance company’s current dividend scale, a corporate investment tax rate of 50.17% (Ontario rates), and a shareholder dividend tax rate of 45.30%.

For the guaranteed investment certificate (GIC) we will use an average of 4% guaranteed interest return every year (generous in the current interest rate environment). (See Table 1, right.)

Deposits of $100,281 per year for 10 years into a guaranteed interest-bearing vehicle. Investment growth averaging 4% rate of return in a corporate account. Tax on investment income is the corporate rate of 50.17%. Investment balance is the remainder after-tax paid. Net to shareholder estate is the net amount when taken out of the holding company as a dividend (45.30% dividend tax).

(Note: Bob does not own the GIC per se; rather he owns the shares of the holding company. Therefore, the deemed disposition and the gain is the Fair Market Value (FMV) of the shares of his holding company less the shares of the Adjusted Cost Base (ACB). In most cases, the shares of an individual’s holding company have nominal ACB.

(See Table 2 on the next page.)

Deposits of $100,281 per year for 10 years into a corporate-owed, tax-exempt insurance plan using a highly rated Canadian insurer’s current dividend scale (dividends are not guaranteed and will vary depending on the company’s future dividend scale).

The corporation would own and pay for the plan and be named as beneficiary (otherwise potential taxable shareholder benefits could arise). Every year for a maximum of 10 years, Bob would simply move $100,281 from his corporate account to fund his new tax-exempt insurance plan. Since he is using tax-paid money from within his holding company to pay the insurance premiums, then there is no tax payable on such payments.

This strategy creates an immediate tax-free estate of $1.5 million. After one year, the policy death benefit grows to $1,614,147. The net amount to the estate consists of the insurance portion that flows tax-free to the company’s CDA, which is then added to the amount that will be released as a non-eligible taxable dividend. The total net value on death would equal $1,569,132 after the first year then continue to grow.

At age 85, the Adjusted Cost Base (essentially the capital invested minus the net cost of pure insurance) of the insurance policy would reach zero, which means Bob’s heirs would receive the total death benefit of $5,722,326 tax-free.

At age 85, the Adjusted Cost Base (essentially the capital invested minus the net cost of pure insurance) of the insurance policy would reach zero, which means Bob’s heirs would receive the total death benefit of $5,722,326 tax-free.

This insurance plan also has a tax-deferred cash value component. At age 65, the cash value would be around 1.6 million. If Bob’s corporation withdraws the cash value, the corporation will pay tax on any accrual gains. The amount of $830,871 is the amount remaining if he withdraws the cash using a non-eligible dividend tax of 45.30%.

Note: A more tax-effective alternative to releasing the cash values would be using the policy as collateral and direct the bank to make Bob a loan. The loan could be tax-free retirement income if set up properly and avoid becoming a taxable benefit to him.

The net to shareholder estate column shows the after-tax amount remaining when withdrawn from a corporation. Bob would be able to access his investment by withdrawing the funds out of his corporation. The GIC has higher after-tax cash values in the beginning and would be taxed annually on income and the growth taxed on death. By comparison, when Bob reaches age 65 and beyond the insurance cash values surpass the GIC investment. The cash values would not be taxable on the growth and would reduce Bob’s annual taxes payable. Options to access his cash values: collateral loan, policy loan, or policy withdrawal.

Table 3 highlights the main advantage when investing in the insurance plan— the amount available to the estate on death. If Bob lived to the age of 85, his corporate GIC would have grown to $2,023,925. Upon his death, the net amount remaining to his estate would be around $1,450,871 (taxable dividend equals $2,652,414, which includes Refundable Dividend Tax on Hand credit, tax payable $1,201,544, estate after-tax, would be around $1,450,871).

With the insurance plan, the amount paid to his estate would be $5,722,326. The taxable dividend (ACB) would equal zero and a tax-free dividend of $5,722,326 flows tax-free to his estate.

The insurance advantage to his estate is quite substantial at $4,271,455.

Note: In general, when someone dies there is a deemed disposition of the shares in their holding company. Therefore, there would be a capital gains tax at death on the Fair Market Value (FMV) of the holding company. The gain is reported on the deceased’s final tax return and payable by the estate. The assets are then transferred to their beneficiaries. To avoid double taxation on the distribution of the GIC you have to look at post-mortem planning. It is important that the business owner’s professional advisors be involved when making these decisions if winding up an estate. It really depends on each situation and the planning done at death. With proper planning using redemption and loss carry-back as well as pipeline planning, you could have a net result of removing either the dividend or capital gains taxation at death respectively.

Conclusion

Despite the regulatory changes, corporate-owned insurance continues to be an excellent tax-advantaged investment option for Canadian corporations. Investing in corporate-owned insurance significantly reduces the amount of tax that a company pays on its investment earnings. In addition, the death benefit immediately increases the value passed on to heirs since it flows tax-free through the company’s capital dividend account.

Investing in traditional guaranteed products, such as GIC’s, could result in at least one-third of business assets ending up going to Canada Revenue Agency on death if there is no spousal rollover provision. Much will depend on the type of post-mortem planning done.

If the intention is to reduce your corporate tax bill, manage risk, and leave most of your corporate assets to immediate family members, then a tax-exempt insurance plan will continue to be an important part of an overall estate plan.

Rino Racanelli is an independent insurance advisor in Toronto. He can be reached by email racanelli@sympatico.ca.