Money and Currency 101: What you don’t learn at School!

Money and Currency 101: What you don’t learn at School!

Money and currency are right now less predictable, more complex, more chaotic, and paradoxically therefore more needing to be understood than at any other time in human history. To understand the complex situation we have now, we need first to go back to basics to understand it all. What is “money”, really, and why do we have another word for it, “currency”?

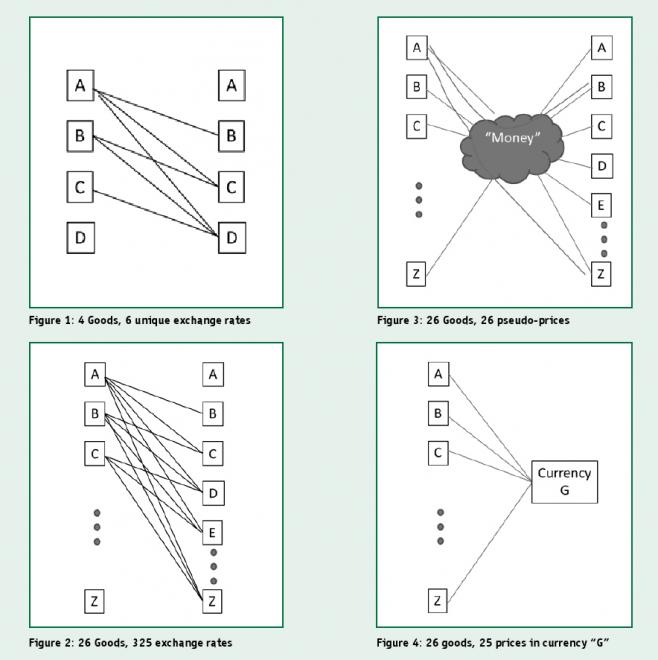

The funny thing about money is that it is just an idea, the idea of “the centre of value” for all goods in an economy. Consider a super-simple moneyless market economy that trades in just 4 goods, labeled A through D, as shown in Figure 1. Here we need just 6 barter-exchange rates to trade everything, noted by lines between the letters (no-one trades A for A, etc – duplicates and inverse ratios are unnecessary and not shown). Line A-C might represent how many ducks per plasma wide-screen TV, B-C how many geese. We observe that as the number of goods increases, the number of relationships increases much faster: for 26 goods we need to know 325 different exchange rates (Figure 2). But by simply placing a reference point in the middle, let’s call it “money”, we only need 26, as shown in Figure 3. To find the fair barter exchange ratio between two goods, we just multiply their money-ratios (“prices”) together. Now, to make it real, and practical, let’s take one of those goods, G, say, and place it in the middle. Now we can understand our entire market with only 25 prices in Gs (Figure 4), plus we have something real we can trade with and use as physical money, namely the good G. This thing (or things) we place in the middle we call currency.

The money-idea and the real currency G solves for us another nasty problem that barter presents. What if I have ducks, and want a plasma wide-screen TV, but the plasma-screen merchant is picky, and needs geese but not ducks? We need something to be money for us, or trade is simply too complicated. Using currency, our plasma-merchant can buy his own geese – I don’t need to find them for him. Money is a very powerful idea, and currency’s value comes from the simplification it offers.

Complex Situations

But even after money, through currency, has simplified things, markets and trade still get complex, so let’s delve into complexity and chaos theory to understand the fate of our fowl. Much as relativity theory rocked the physics world, and quite literally the real world, complexity theory is now rocking all scientific disciplines, including economics. The theory points to two key outcomes.

The first is that complex systems obey power-law rules, not the “normal” Gaussian distribution that we came to know and hate in our statistics and risk-analysis courses. The big difference here is that power-law based systems have outcomes with “fat tails” that give rise to “black swans”: there are bigger chances of wild outcomes. Further, chaotic power-law systems exhibit a property known as bifurcation, where the system can suddenly change its behaviour by moving from one set of steady states (a “strange attractor” in complexity-speak) violently to another set. The occurrence of these shifts is not necessarily predictable or time-able, though we get hints.

Secondly, and more interesting yet is the emergent order in complex chaotic systems. The best way to understand this in terms of economics is to read “ I, Pencil”, written in 1958 by Leonard E. Read. (Read "I, Pencil" here.)It also applies to currencies in some cases. What Mr. Pencil has to say (and not just about pencils, but all goods, including currency-goods) is that we can’t know why, exactly, we arrived at pencils as our solution to writing efficiently, nor can we know how to build a pencil, as that can only be done by the market-at-large. The information with which to build the modern pencil emerged inside the market, not within us, and each of us can only understand a little bit of it, never all. You can’t write it down, or explain it. A complex system like a market can “choose” to make pencils and “learn” how to make them better. It can “decide” to make them differently, has, and does. It can do the same thing with currencies. Our ecosystems have done all this for millennia, and the ecosystem is very good at making trees, birds, all kinds of things. At the system level, there are not many differences between ecosystems and markets.

Serious Currency

So we can’t know exactly why, but for some reason, quite early on and for several thousand years - most of our civilized life in fact - man’s markets have chosen precious metals as their preferred currency. There are certainly exceptions, for instance in Canada we have had axe-heads, beaver-pelts, wampum, chopped-up autographed playing cards(1), as well as so many competing metal coinages circulating at the same time that we had our own set of exchange-rates, the Halifax Ratings of 1758. But in terms of all these goods-based currencies, gold and silver have always been preferred because their attributes serve the money-function so well.

Currency must be relatively scarce (stuff that is plentiful has little economic value), durable, divisible, portable, easily authenticated, and the metals possess all these attributes. Gold, silver, and copper are also terrifically valuable for their ductility, malleability, and as the best conductors of heat and electricity, thus only part of their value is currency-value. Had gold and silver not been rendered “expensive” because of their extreme utility to the market as currency, rest assured their use in all sorts of applications would be guaranteed. In fact, it is possible that the market long ago “understood” this, and selected these metals precisely because of their limited-supply and ubiquitous potential application. We can never know, but I don’t consider it coincidental that all our monetary metals come from the same column in the periodic table of the elements. To my sisters who ask “Why gold?” I could only reply “Why tree?” They are the same question. Same answer, too: “because it works.” (2)

What is currently currency?

Paradoxically, perhaps, that we now have paper currency is due to the gold-bankers. In the 17th century British and Dutch merchants grew tired of lugging around bags of coins (and getting mugged), so a market developed for safe gold-storage, for which transferrable receipts were issued and these entered circulation in payment for goods. Not long after, that very first clever banker, who, upon noticing that not everyone showed up for their gold at the same time, issued just one extra receipt in the form of a loan, created fractional-reserve gold-backed banking, and it lasted a long time. The paper receipts morphed into bills and notes, banks came and went again if they ran the reserve too low, but in general, notes were redeemable on demand in gold for many, many decades.

In fact, most of the 200-year industrial revolution, an era of unprecedented innovation, prosperity and financial stability occurred under a gold-standard monetary regime. But what benefits innovators, individuals and industry does not necessarily equally reward bankers and bureaucrats.

So things changed – I would argue for the worse – in the early 1900s when central banking took the world by storm, and the industrial revolution was ground to a halt. Until then, things had been a bit chaotic, it is true, but it does turn out that chaos is a part of nature. Most money-historians point to a meeting of bankers and dignitaries at Jekyll Island in 1908 as the turning point, after which central-banking legislation was enacted in many countries, in the US in 1913, Canada in 1914.

The theory was that to ensure bank stability – there had been runs and failures, mind you! – What was needed was a “lender of last resort” to whom a fractional-reserve gold-backed bank with a sound balance sheet but a temporary liquidity-crunch could appeal so that the bank’s outright failure might be averted. Unfortunately, chaotic systems don’t much like being controlled, and they bite back, as they did in 1929, and through the 1930s, and again now.

International Trade and Currency

Before moving on to the next step in the evolution of our money – and it truly is evolution, though selection is not quite natural – we need to talk about trade. In times when only precious metals were used to settled international trade, there was no need for currency exchange rates, per se, as one would simply compare weights of pure metals. But paper currency, redeemable into gold only locally in a country or region, changes the picture. There are some things that must balance when currency-regimes trade. The net flow must be zero. If goods go one way, currency has to move the other. If a country tries to create a currency other than gold, and then buy more stuff than it makes using it, those dollars, say, are going to eventually come home as foreigners can’t spend them locally, nor convert them to gold. And when they return, the exchange rate drops. Long term, it is a zero-sum game, and US dollars have been flowing out for decades now.

Reserves of gold, in the old days, or trading-partner fiat-currency in our times, are held in reserve by central banks so that goods entering the country can be paid for, and international accounts settled, so then further trade can occur. Until the 1930s, this tended to occur bilaterally, but gradually the Bank of International Settlements, formed in 1930 to deal with Germany’s WW I reparations, assumed the role of the single overarching global central bank. It still is (though it is suspiciously absent from media coverage!).

Trade was seriously disrupted by World War II, as were flows of gold and currency to settle the trade that did occur. The solution presented to this and other trade and currency problems was the Bretton Woods agreement of 1944 in which it was decided that the US Dollar would replace gold for the settlement of international trade. At the time it was redeemable for gold by foreign central banks, but not US citizens, who lost that right in 1933 when dollar redemption and private gold ownership were revoked and the dollar depreciated from $20.67/oz to $35/oz overnight.

This all worked until 1971, when the US, having printed too many dollars in support of Bretton Woods, and not wanting to ship all their national gold reserves abroad, suspended all redemption into gold. The French were the last to get gold for their dollars at the set rate. Support for the value of the US dollar was maintained thereafter through the artifice of enforcing oil transactions in US dollars, thus necessitating demand by all who, say, want to drive or stay warm. The US dollar still clings to value as a global reserve, but tenuously.

Canada’s money now

I remember as a youth learning about money reading the words “Pay to the Bearer on Demand” on our Canadian bills, and noticing the words disappear in 1969, and seeking to understand what that meant. I now understand. Our money-concept currency-placeholder today, the “dollar” is created solely by act of fiat. It is simply a promise by all Canadians to each other and to foreigners, imposed upon us by the government we elect, that we will accept the currency for our goods and services. Further we are required to submit our taxes in this currency. We expect others to honour it, but we can no longer demand of our banks that they produce a fixed amount of real money, i.e. gold or silver, when presented with bills. This is a recent development. I can remember it happening.

Debt-money

Our currency is now created by debt. Our supply of currency is created initially by the Bank of Canada when it issues currency and buys with it Government of Canada debt. Only a small fraction, perhaps 5% of Canada’s money is created this way. The rest is created when we enter into debt with the banks. When I get a loan, the bank creates two entries on its balance sheet, an asset – my debt, and a liability - the demand-deposit balance that lands in my account. And money (strictly, currency) is thus created as the balance sheet expands. Amazing, isn’t it? Yet that truly is how our money supply is now created. I will leave it as an exercise for the reader to figure out from whence comes the extra money needed to pay the interest on the money borrowed in a previous period.

Inflation and deflation: the truth

Inflation of our money supply now occurs when individuals, corporations, or governments borrow money in Canadian dollars. It contracts when debts are re-paid or worse, when defaults occur. It is an interesting comment on the degree to which we have come to blindly accept the current system that Canadians now almost universally associate inflation and increasing price levels with an advancing economy. In fact, the opposite is true, all else equal. As an economy grows it only does so if it can learn more efficient ways to get things done through specialization. Specialization only occurs if it is less costly. Less cost means lower price. In a stable-currency economy, there is an inherent downward pressure on almost all prices. Not just VCRs get cheaper. The only reason prices keep going up in dollars now is that we keep incurring more debt. Don’t forget your homework assignment above!

The, Ahem, Current International Situation

Enough theory. What is going on now? This summary was not intended to scare you silly. Canada fortunately has had some of the best banking (and thus currency)

practices in the world. But the facts are chilling when summarized:

- Fiat currencies and central banking now dominate the globe. This is unique in human history. All previous fiat currencies have failed, most of them spectacularly so;

- Money supplies (and debt levels everywhere) are enormous, and under enormous pressure in both inflationary and deflationary directions;

- Many debtors, including individuals, cities, counties, states are essentially insolvent when the current value of future obligations are considered;

- Governments everywhere are under intense pressure to issue debt and create money to bail out failing financial institutions;

- Insolvencies and default are moving from private failures (Long Term Capital Management, Bear Stearns, Lehman Brother, MF Global off the top of my head) to sovereign failures (Iceland, Ireland, Greece, and onwards)

- In addition to conventional debt, the opaque over-the-counter derivatives market has put orders of magnitude more leverage into the banking system, a very destabilizing influence;

- In the US and internationally, the rule of law in finance is being largely overlooked, some might say it is in tatters;

- TheUS dollar, as shaky as it is, is still the primary tool for international trade settlement;

- The Euro, perhaps created to compete with the US dollar in that role, is either doomed or the governments within it are. One cannot have common monetary and disjoint fiscal policies and trade balances amongst sovereign nations. It can’t work, as there is no way for the complex system to balance itself;

- The Bank of Canada has virtually no gold reserves;

- Canada maintains a strategic reserve called the Exchange Fund Account of primarily US dollars, Euros and Yen to ensure the continuity of trade, with just 0.25% in gold.

Science is now at odds with the possibility that central banking provides stability. We now know that central control paradigms on complex systems may have a short- term stabilizing effect, but that this can only be achieved at the expense of much greater (though perhaps less frequent) instability as the system shifts to a different strange attractor as it rejects the control offered. There is only a certain amount of certainty in nature, and we cannot cheat.

A sign that a state-change in our financial system might be imminent is when things start to get very correlated, when everything either goes up, or it all goes down, everywhere, at the same time. This was evident before fall 2008, and it is evident again now as the HSBC correlation index is at an all-time high2. In 2008 what were previously uncorrelated asset classes - stocks, bonds, commodities, real estate - all began to move in unison. That is the sign that the market is changing its mind about its money.

What Can You Do About It Personally?

What one chooses to do about all this depends on what one expects this now highly unpredictable currency- system to do. It is not impossible that fiat currencies yet persist for some time, that voters vote for austerity, governments develop fiscal prudence, citizens bear down, pay off personal debt, pay higher taxes, and accept reduced government benefits, and we then might have a period of deleveraging to slowly but very painfully unwind the world from our current position while maintaining our faith in fiat. Currency would be the best asset to own in this slow deflationary scenario. I don’t think it is likely.

It is more probable that the band-aid will be torn off quickly by the market, and the US dollar and the Euro will vie for the lead in the battle for the bottom. While governments and bankers may try to manage a gentle de-leveraging, in examples from history the market has been savage. Typically, the attempts to sustain a fiat status quo involve monetary inflation (and then the unintended hyperinflation) as the means to “solve” the debt crisis in the local currency. If one were certain of the inflationary scenario, debt would be the best thing to have, provided one also possesses inflation-proof hard assets, and/or inflation-indexed income, so that one can meet interest payments.

Short-term predictions are even more difficult in this system, as crowd behaviour will lead to such paradoxical effects as rushes to US treasuries as a “safe haven” despite what seems an obvious inability for the US to do anything long term but inflate away their global obligations. While the US remains our largest trading partner and we link our currencies through the reserve mechanism Canadians will to some extent get taken along for the US ride.

In my opinion, in a great de-leveraging the most sensible thing to do is to own some of the most real form of money you can, precious metals. Individual miners or mining funds are an option, to own metal-in-the-ground, but as insurance against global financial calamity, watch out for sovereign risks. Countries play gold close to the chest once trouble hits. If you hold securities “in street name”, you are dependent on the solvency of your finan- cial institution. If you believe that the financial system will persist with derivative assets intact, one could buy GLD or SLV, but know that these will likely be early casualties of a state-change. Better yet might be one of Sprott’s PSLV or PHYS, or CEF, or BMG, or other Canadian bullion funds.

The best currency-insurance you can get? Physical metal, in your possession. Premiums for physical metal over the “spot” or other “paper-metal” prices are only going up.

The other important thing you could do is to write our politicians, tell them you now understand how our monetary system currently works (or not!), that you don’t like it, and that we need to get back to gold or another market-tested metal to restore financial faith.

And if they ask you “Why gold?” Ask them right back “Why tree?

1. Seriously, In 1685, Jacque de Muelles, Intendant of Justice, Police, and Finance for New France found himself without funds to pay his soldiers. After exhausting local sources of borrowed currency, he finally cut a deck of cards in pieces, initialed each piece, and paid his troops with them. These entered circulation as currency. Card-money was again issued in 1686 and 1690, circulated freely until 1714, and was finally redeemed and retired in 1717. From A History of the Canadian Dollar, James Powell, Bank of Canada, 2005. The full text can be found at: http://www.bankofcanada.ca/publications-research/ books-and-monographs/history-canadian-dollar/

2. https://www.research.hsbc.com/midas/Res/RDV?p=pdf&key=2Q 70z09rbF&n=282506.PDF

by Ben Bacque, Canadian MoneySaver contributor

Ben’s interest in economics and investing began in his teens, trading equities on the TSE in the late 1970s. After receiving bachelor’s and master’s degrees from the University of Toronto in Engineering Science and Electrical Engineering, Ben pursued a career in telecommunications in Ottawa. Having co-founded Tropic Networks in May 2000, Ben went on to lead Tropic in product, technology, and R+D management through the mine-fields of the tech bubble bust until acquisition by Alcatel-Lucent in May 2007. After ensuring a successful transition of product, customers, team, and technology into the ALU fold, Ben has now spent sev- eral years “on sabbatical”, consulting and pursuing personal interests, especially in the areas of political economy and economic history, bringing his systems-theoretic perspective to bear. Ben currently lives in Ottawa, but is always happiest when sailing with his family on the Georgian Bay. Ben can be reached at jbbacque@gmail.com