When Financial Advice Fails You: What To Know In 2026

Most financial planning articles provide a standard roadmap for different life stages: save early in your 20s, maximize Registered Retirement Savings Plans (RRSPs) in your 40s, and plan for your retirement income in your 60s. This is sound foundational advice. However, what these articles often omit is a critical factor in your long-term success: understanding whether the advice you receive is designed for your benefit or for the business interests of the provider.

I spend too much of my time examining the machinery of Canadian financial regulation—identifying where it supports consumers and where gaps remain. While recent reforms have introduced more transparency, the difference between the protection you assume you have and the protection you actually have can still be large.

In 2026, our regulatory system is still a patchwork of federal and provincial rules, varying by product type and advisor category. While the system has genuine strengths, it also has limitations that shift as you age. This article examines the current landscape so you can make truly informed decisions—not just about your investments, but about the professional standards of the advice itself.

The 20s And 30s: Choosing Your Advice Model

Your 20s and 30s are the most critical building blocks of your financial life. This is the time to get started, but the most important decision you will make is not which stock to buy—it is identifying which investment model actually suits your needs. The choice you make today about how you receive advice can determine whether hundreds of thousands of dollars stay in your pocket or migrate to your advisor's firm over the next forty years.

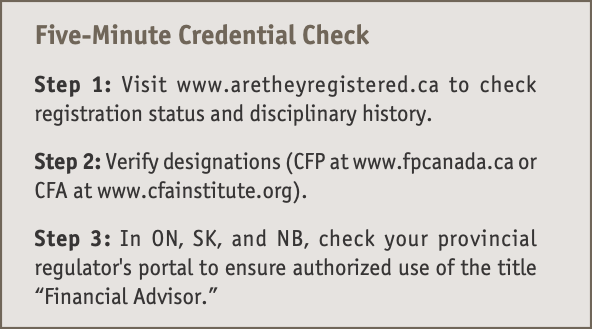

Selecting that model, however, is easier said than done because the industry labels can be confusing. In 2026, for example, legislation in Ontario, Saskatchewan, and New Brunswick requires individuals using titles like "Financial Advisor" to hold approved credentials. While this sounds like a safeguard, the title is less important than the registration category, which dictates the "model" of advice you are receiving.

Most branch-level professionals are registered as "Approved Persons". They operate under a suitability model. Their legal duty is to ensure an investment fits your basic profile, but they are not required to search the market for the best or lowest-cost option. Contrast this with Portfolio Managers, who work under a fiduciary model, legally prioritizing your outcome over their own commissions.

The key is informed choice. In the suitability model, you are in a "service-for-sales" relationship—you get advice in exchange for buying that firm's products. In the fiduciary model, you are paying for professional management in which the advisor's only loyalty is to your bottom line. You can figure out which model you are in by visiting www.aretheyregistered.ca. If the status says, "Dealing Representative," you are in a suitability/sales model; if it says, "Advising Representative" or "Portfolio Manager," you are in a fiduciary model.

The Real Impact of Cost:

Imagine you are 28 with $100,000 to invest.

- Suitability Model: A "suitable" mutual fund with a 2.0% annual cost.

- Fiduciary/Low-Cost Model: A diversified ETF portfolio with a 0.3% annual cost.

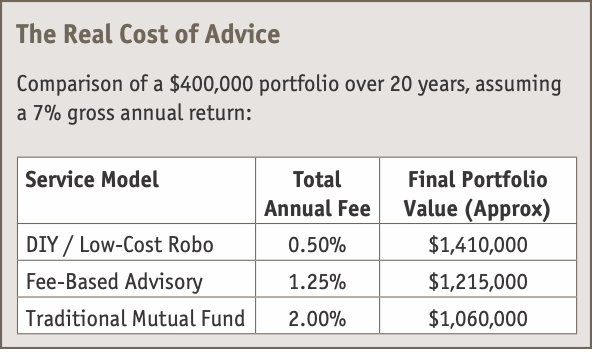

Assuming a single $100,000 lump-sum investment, no additional contributions, and a 7% average annual gross return — figures used for illustration purposes only — that 1.7% fee difference results in approximately $265,000 in lost wealth over 30 years. Both models are legal, but only one maximizes your after-cost returns. Your actual gap will vary depending on contribution frequency, account type, and return assumptions. To model your own situation, use the Ontario Securities Commission fee impact calculator at GetSmarterAboutMoney.ca.

The 40s And 50s: Evaluating Value And Avoiding Complexity

As your assets grow, you will typically be transitioned to "Fee-Based Accounts." In 2026, this is the standard for portfolios exceeding $500,000. Instead of sales commissions, you pay a visible annual fee—typically around 1% of assets.

If you have a $600,000 account, a 1% fee means you are paying $6,000 every year. At that price, it is appropriate to expect your advisor to provide more than just quarterly statements and an annual portfolio review. For $6,000 a year, your advisor should be the "quarterback" of your financial life, providing:

- Asset Location Strategy: Ensuring high-tax investments (like bonds) are in sheltered accounts while tax-efficient ones (like Canadian stocks) are held in taxable accounts.

- Tax-Loss Harvesting: Proactively selling losing positions to offset capital gains, a task that requires year-round monitoring.

- Estate & Beneficiary Audits: Coordinating with your lawyer to ensure your insurance, Wills, and accounts do not conflict, which can save your heirs tens of thousands in probate and legal fees.

The Insurance Trap: Permanent vs. Term

During these peak years, you may be offered Permanent Life Insurance (Whole or Universal Life). Often marketed as a "tax-advantaged investment," these types of insurance are far more complex and expensive than simple Term Insurance. Commissions on permanent policies can exceed 100% of your first-year premium. If an advisor steers you away from Term, ask for a written 20-year cost comparison. Most people find that "buying term and investing the difference" in low-cost ETFs provides significantly more flexibility and higher net wealth.

The 60s and Beyond: Protecting Your Retirement Legacy

In retirement, your focus shifts from accumulation to preservation. This shift makes you a prime target for products designed to appeal to your fear of market loss.

The "Guarantee" Caution: Segregated Funds

Segregated funds are mutual funds with an insurance wrapper. They promise to protect your principal if held for 10 years or upon death. However, this "insurance" usually costs an additional 1% to 1.5% in annual fees. Over a 25-year retirement, that fee drag can cannibalize hundreds of thousands of dollars of your capital. For most retirees, a "bucket" strategy (keeping 2 years of cash in GICs and the rest in low-cost funds) provides similar protection without the high cost.

Immediate Annuities: A DIY Pension

An Immediate Annuity is a contract where you give an insurance company a lump sum (e.g., $200,000) in exchange for a guaranteed monthly paycheque for the rest of your life. It is effectively a "DIY pension."

- The Transparency Gap: Monthly payouts can vary by 10% or more between insurers for the same lump sum.

- The Commissions: These are "baked into" the rate and rarely explicitly disclosed.

Never accept the first quote. Insist that your advisor provide a market survey of at least three different insurers (e.g., Sun Life, Canada Life, Desjardins). If they can only show one, they are not shopping for your best interest.

The Power of Attorney (POA) And The "Trusted Contact"

One of the greatest risks to retirees in 2026 is not the market; it is the potential for financial mismanagement through a Power of Attorney. To protect yourself:

- Appoint a Trusted Contact Person (TCP): A TCP is an individual the bank can call if they suspect you are being coerced or they see unusual patterns. Unlike a POA, the TCP has no power to see your balance or move money. They are your primary "early-warning system."

- The "Second Signature" Rule: Consider requiring two people to sign off on any withdrawal over a certain amount (e.g., $10,000). This creates a check-and-balance system that protects both you and your heirs.

The Empowered Investor’s Manifesto

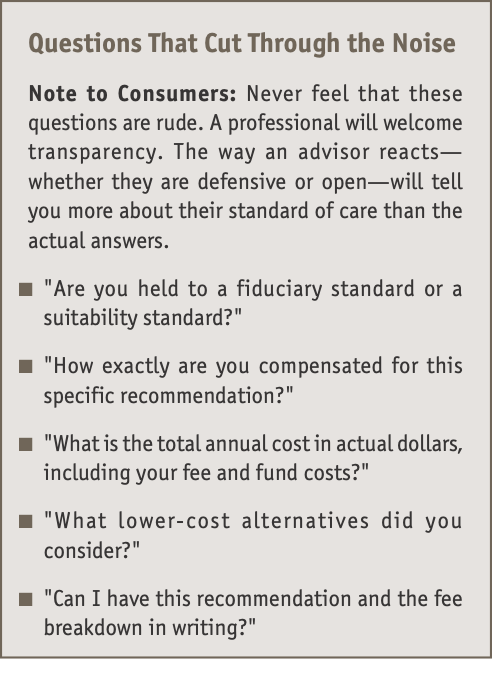

Navigating the Canadian financial system in 2026 requires more than just checking boxes; it requires a shift in mindset from being a "customer" to being a "client." Regulations can mandate that an advisor be "suitable," and can mandate that advisors must "put your interests first" in a general sense. But no regulator can force an advisor to be curious, proactive, or truly cost-conscious on your behalf.

The most effective protection you have is the clarity of your own expectations. If you are paying several thousand dollars a year in fees, you are the employer in this relationship. Demand documentation, ask for lower-cost alternatives, and never be afraid to pay for a second opinion from a fee-only planner who has no product to sell. In a system built on complexity and obscured incentives, your greatest asset is the willingness to ask "Why?" until you understand the answer. Your financial future is not just about the markets—it is about the standards you set for the people who manage them on your behalf.

Consumer Protection Contacts

National and Regulatory & Advocacy Bodies:

OBSI: (Ombudsman for Banking Services and Investments) | 1-888-451-4519 | www.obsi.ca

CIRO: (Canadian Investment Regulatory Organization) | 1-877-442-4322 | www.ciro.ca

FCAC: (Financial Consumer Agency of Canada) | www.canada.ca/en/financial-consumer-agency

Provincial Securities Regulators:

Ontario Securities Commission (OSC): www.osc.ca | 1-877-785-1555

BC Securities Commission (BCSC): www.bcsc.bc.ca

Alberta Securities Commission (ASC): www.asc.ca

Autorité des marchés financiers (Quebec): www.lautorite.qc.ca

Financial and Consumer Affairs Authority (Saskatchewan): www.fcaa.gov.sk.ca

Financial and Consumer Services Commission (New Brunswick): www.fcnb.ca

Manitoba Securities Commission (MSC): www.mbsecurities.ca

Nova Scotia Securities Commission (NSSC): nssc.novascotia.ca

Harvey Naglie is a consumer advocate who regularly comments on the financial services sector. A former senior policy adviser with Ontario's Ministry of Finance, he brings extensive experience in financial regulation and investor protection to his advocacy work, holding an LL.M. in Securities Law and serving on the faculty at McMaster University's Directors College.