How Diversified Revenues Are Powering Investor Interest In Canada’s Big Six Banks

Every earnings season, Canadian bank results invite the same familiar question: How are the banks doing, and what does it mean for investors? This year, that question feels especially relevant. The ETF and Alternatives Strategy team at BMO Global Asset Management has done some analysis on the outlook for Canadian banks, and we’ll be synthesizing their report here.

Economic uncertainty remains elevated, loan growth has slowed to a crawl, and investors are debating whether the Bank of Canada might still be talking about rate hikes sometime in late 2026. Against that backdrop, the latest results from Canada’s Big Six banks might seem surprising to investors: minimal growth in lending didn’t stopped banks from generating revenues. In fact, it’s becoming increasingly clear that Canadian banks have done well to diversify their revenue streams —and that shift has important implications for investment portfolios.

At the end of 2025, the earnings picture was mixed for the big six banks. Traditional personal and commercial lending continued to struggle, particularly in Canada, where higher interest rates and cautious borrowers have dampened demand. Pre tax, pre provision earnings in these segments generally came in softer than expected. But that weakness was more than offset elsewhere. Capital markets and wealth management were the stars of the quarter. Trading desks benefited from volatile markets, while fee based wealth platforms continued to attract assets and generate steady income. Credit quality also remained a focus. Banks took different approaches when assessing future risk, with some increasing provisions for non impaired (Stage 1 and 2) loans.1 That doesn’t signal stress today—but it does show that management teams remain cautious about the economic outlook and are building buffers accordingly. And then there’s the availability of capital. On that front, the story remains positive for Canadian banks going forward.

Strong Capital Is the Canadian Banks’ Secret Weapon

All six major Canadian banks continue to hold capital levels well above regulatory minimums. That gives Canadian banks a lot of flexibility and some have used that opportunity to increase dividends and conduct share buybacks. That is welcome news for income oriented investors. But that flexibility also extends to the ability to deploy capital when opportunities arise, absorb potential credit losses, and invest in higher growth, fee based businesses. This is a big reason why Canadian banks have been able to navigate a challenging environment better than many expected.

The Bigger Story: Banks Are Less About Lending Than Ever Before

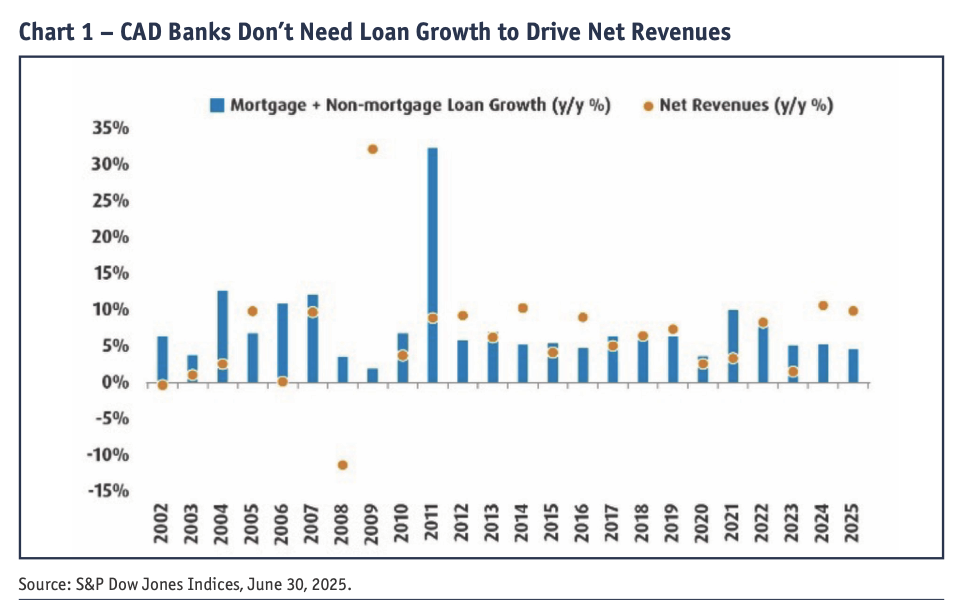

If there’s one unifying theme we learned from reviewing recent bank earnings, it’s this: Canadian banks are no longer just lending machines. Consider the data. Loan growth—both mortgages and non mortgage lending—is on track to be the slowest in a non crisis year since the early 2000s (excluding the financial crisis and the pandemic). By historical standards, this is a remarkably weak lending environment. Yet despite that headwind, bank revenues grew by nearly 10% year over year —one of the strongest revenue growth years this century. How is that possible?

The answer lies in diversification. Trading revenue, wealth management fees, insurance income, and other non interest sources now account for roughly 54% of total bank revenues. For much of the past two decades, that figure sat below 50%. Today, more than half of bank revenue comes from activities that don’t require loan books to grow at all.

This shift matters. Fee based income tends to be more scalable, less capital intensive, and—over time—more resilient than traditional lending. It’s a structural change that has helped Canadian banks maintain profitability even as loan growth has stalled.

What Could Drive The Next Leg Of Growth?

For Canadian banks in 2026, there are several potential tailwinds. Public private partnerships tied to federal infrastructure, housing, and defense initiatives could increase demand for capital. A lower starting point for interest rates may help stabilize housing markets and gradually revive mortgage activity. And if trade negotiations under a renewed CUSMA (Canada-United States-Mexico Agreement) framework proceed smoothly, business confidence and investment could improve. Importantly, banks don’t need all of these things to go right to keep generating returns. Their diversified revenue base and strong capital positions give them multiple paths forward.

The Valuation Question

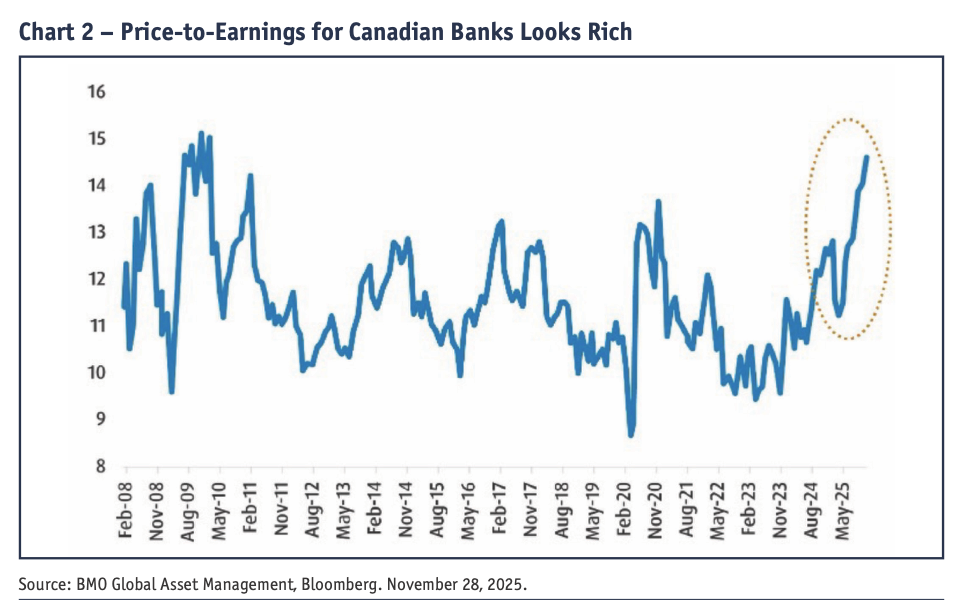

That said, no investment story is complete without addressing valuation—and this is where some caution is warranted. Canadian bank stocks have been trading at relatively rich valuations compared to historical averages. That doesn’t mean they’re destined to fall, but it does suggest that future returns may be more modest and potentially more volatile than investors have become accustomed to. For investors who remain constructive on the sector but are uneasy about valuations, this environment may favour strategies designed to smooth returns.

Positioning Portfolios For Today’s Bank Environment

From an investment standpoint, the takeaway is straightforward. The Canadian banks’ strong capital positions continue to support dividends and buybacks, making the sector attractive for long term investors seeking income and stability. For those looking for broad exposure without betting on any single bank, an equal weight approach like ZEB, the BMO Equal Weight Banks Index ETF, offers diversified access to the group and avoids concentration risk. For investors more sensitive to valuation risk or near term volatility, covered call strategies such as ZWB, the BMO Covered Call Banks ETF can provide enhanced income potential while helping to dampen price swings.

Bottom Line

Canadian banks may be facing the slowest loan growth in decades—but they’ve proven that loan growth is no longer the sole driver of success. Diversified, fee based revenues, disciplined risk management, and fortress like capital positions have reshaped the sector. For retail investors, that evolution changes the conversation. The question is no longer whether banks can grow without lending—but how best to gain exposure to a sector that has learned how to do exactly that.

Saakshi Mehta joined BMO Global Asset Management in October 2025 and currently serves as Vice President, ETF and Alternatives Strategy. Her work focuses on macroeconomic trends and their implications for ETF markets, including analysis of monetary policy, fiscal developments, and market structure across asset classes. She holds a Master of Financial Economics from the University of Toronto and a Bachelor of Arts in Economics and Psychology from the University of British Columbia.

1 A Stage 1 Loan is a loan with no significant increase in credit risk since initial recognition, or a low-risk loan. A Stage 2 Loan is an underperforming loan which carries increased credit risk) since initial recognition, but is not yet in default.

Disclaimer:

The BMO ETFs sponsored articles are intended for information purposes only. They have been prepared by the respective authors and represent their assessment at the time of publication. The comments herein do not necessarily represent the views of BMO Global Asset Management. The views are subject to change without notice as markets change over time. The information contained herein does not constitute a solicitation of an offer to buy, or an offer to sell securities, and should not be construed as investment, tax or legal advice to any party. Particular investments and/or trading strategies should be evaluated and professional advice should be obtained with respect to any circumstance. Past performance is no guarantee of future results.

Any statement that necessarily depends on future events may be a forward-looking statement. Forward-looking statements are not guarantees of performance. They involve risks, uncertainties and assumptions. Although such statements are based on assumptions that are believed to be reasonable, there can be no assurance that actual results will not differ materially from expectations. Investors are cautioned not to rely unduly on any forward-looking statements. In connection with any forward-looking statements, investors should carefully consider the areas of risk described in the most recent simplified prospectus.

Commissions, management fees and expenses all may be associated with investments in exchange-traded funds. Please read the ETF Facts or prospectus of the BMO ETFs before investing. Exchange-traded funds are not guaranteed, their values change frequently and past performance may not be repeated. For a summary of the risks of an investment in the BMO ETFs, please see the specific risks set out in the prospectus. BMO ETFs trade like stocks, fluctuate in market value and may trade at a discount to their net asset value, which may increase the risk of loss. Distributions are not guaranteed and are subject to change and/or elimination.

"The Select Sector SPDRÆ Trust consists of eleven separate investment portfolios (each a “Select Sector SPDR® ETF” or an “ETF” and collectively the “Select Sector SPDR® ETFs” or the “ETFs”). Each Select Sector SPDRÆ ETF is an “index fund” that invests in a particular sector or group of industries represented by a specified Select Sector Index. The companies included in each Select Sector Index are selected on the basis of general industry classification from a universe of companies defined by the S&P 500Æ. The investment objective of each ETF is to provide investment results that, before expenses, correspond generally to the price and yield performance of publicly traded equity securities of companies in a particular sector or group of industries, as represented by a specified market sector index.

The S&P 500®, SPDRs®, and Select Sector SPDRs® are trademarks of The McGraw-Hill Companies, Inc. and have been licensed for use. The stocks included in each Select Sector Index were selected by the compilation agent. Their composition and weighting can be expected to differ to that in any similar indexes that are published by S&P.

The S&P 500 Index is an unmanaged index of 500 common stocks that is generally considered representative of the U.S. stock market. The index is heavily weighted toward stocks with large market capitalizations and represents approximately two-thirds of the total market value of all domestic common stocks. The S&P 500 Index figures do not reflect any fees, expenses or taxes. An investor should consider investment objectives, risks, fees and expenses before investing.

You cannot invest directly in an index.

An investment in Canadian depositary receipts (“CDRs”) issued by Bank of Montreal (“BMO”) may not be suitable for all investors. Important information about these investments is contained in the short form base shelf prospectus and prospectus supplement for each series of CDRs (together, the “Prospectus”). Purchasers are directed to www.sedarplus.ca or to bmogam.com to obtain copies of the Prospectus and related disclosure before purchasing CDRs. Each series of CDRs relates to a single class of equity securities (the “Underlying Shares”) of an issuer incorporated outside of Canada (the “Underlying Issuer”). For each series of CDRs, the Prospectus will provide additional information regarding such series, including information regarding the Underlying Issuer and Underlying Shares for such series. Neither BMO and its affiliates nor any other person involved in the distribution of CDRs accepts any responsibility for any disclosure provided by any Underlying Issuer (including information contained herein or in the Prospectus that has been extracted from any Underlying Issuer’s publicly disseminated disclosure). Each series of CDRs is only offered to investors in Canada in accordance with applicable laws and regulatory requirements.

Commissions, management fees and expenses all may be associated with investments in exchange-traded funds. Please read the ETF Facts or prospectus of the BMO ETFs before investing. The indicated rates of return are the historical annual compounded total returns including changes in unit value and reinvestment of all dividends or distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any unitholder that would have reduced returns. Exchange-traded funds are not guaranteed, their values change frequently and past performance may not be repeated.

BMO ETFs are managed by BMO Asset Management Inc., an investment fund manager, a portfolio manager, and a separate legal entity from Bank of Montreal. BMO Global Asset Management is a brand name under which BMO Asset Management Inc. and BMO Investments Inc. operate.

BMO (M bar roundel symbol) is a registered trademark of Bank of Montreal, used under licence.