Launch Money: Considerations For Helping Children With Homeownership

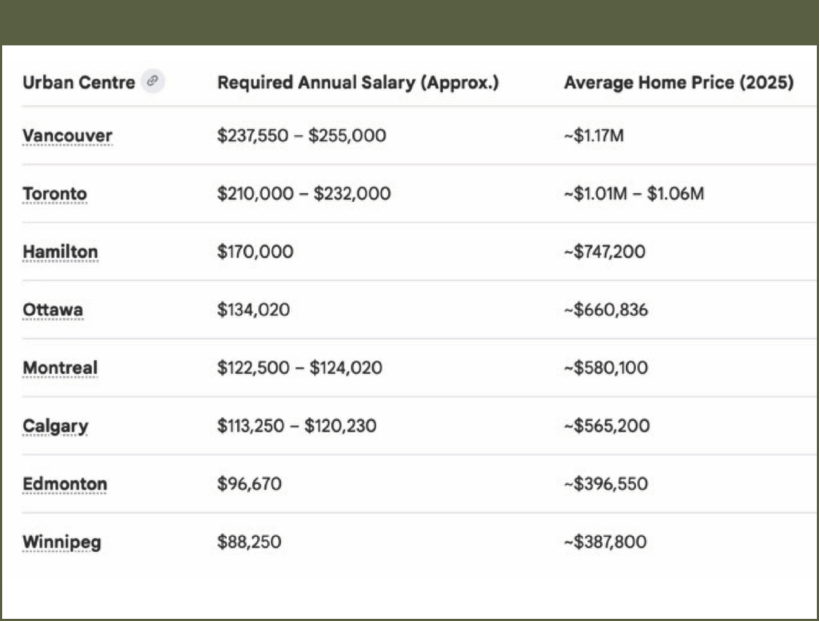

For younger Canadians, it’s never been more challenging to get into the housing market. Despite the dream, the reality is that rates of home ownership are falling sharply, with nearly a quarter of Canadians ages 18 to 34 owning a home today, down from nearly 50 per cent in 2021. Beyond the down payment, keeping up with mortgage and maintenance costs is becoming more onerous. Mortgage default rates for under-30s are seven times higher than for the rest of the population, based on data from TransUnion.

According to a recent Ipsos poll, 78 per cent surveyed said that owning a home in Canada is only for the rich. Indeed, a report from Statistics Canada on people born in the 1990s showed that those whose parents are residential homeowners were twice as likely to own a home themselves as those with parents who were non-homeowners, keeping constant the adult children’s incomes, ages, and provinces of residence. When parents own multiple properties, their adult children are also more likely to own multiple properties compared to their peers.

Parents and grandparents recognize that their younger family members need financial support to gain a perch in the residential real estate market. The share of first-time homebuyers who receive a financial gift has risen, and so has the average amount gifted, says Lorne Rapkin, CPA, partner at Rapkin Wein LLP, a Toronto-based consultancy firm.

“We’re seeing more help from parents and grandparents. Property values, especially in places like the Greater Toronto Area, have become very challenging for any young, professional couple to get into the market. Parents who have done the financial planning and know what they need to live off are more likely to move the excess amount to younger relatives,” he said. “They’d like to see their families enjoy it while the parents are still alive. Also, at a 53 per cent tax rate, if the parents don’t have a good life insurance policy to cover the liability, they are more likely to offload to younger family members within their lifetimes as part of the estate plan.”

Gillian Oxley, Toronto-based founder of Oxley Real Estate, a top-ranked Canadian agency, is seeing this changing mindset firsthand. “Parents are not holding onto the money as long as they used to,” says Oxley. “I have a client family with one daughter, and they’re buying her a $500,000 condo as a gift. When I was growing up, there was only one girl in school whose wealthy parents bought her a house when she got married, which was very atypical at that time. Everyone else just had to wait.

“There used to be a mindset of starting small by buying a condo or fixing up a small house, then selling it and rolling the money into a better property and so on. My first home cost $210,000, and finding that extra $10,000 for the down payment was a huge stretch. I wasn’t too savvy; I put it on my Visa. Today, young people are much savvier, but it’s harder to get into the city centre unless you have access to the Bank of Mom and Dad,” said Oxley. “Family members want to help the next generation get into the housing market because there is still a strong belief that home ownership represents stability. During open houses, I’ll often see parents or grandparents as the scouting party.”

Providing financial support to younger relatives is increasingly common, but well-meaning parents and grandparents should be aware of dos and don’ts when giving gifts, and, despite how helpful ChatGPT can be, they should always consult a legal or tax professional before making a big decision.

“In Canada, you can gift as much as you want, and there is no time frame for gifting,” says Rapkin. “Just make sure a gift letter is in place. In our practice, we always plan for the worst-case scenario, so the gift letter should protect the inheritance in the event something happens in your child’s marriage, for example. While you could certainly get ChatGPT to draft it, you’d still want to ensure certain clauses and elements are in the document. The most important thing is to specify the purpose—buying a home.”

When giving a cash gift, parents need to consider the tax implications. If there is a sale of assets with capital gains, then the parent is liable for paying the taxes, thus reducing the net value of the gift. One strategy for those with a private corporation that contains assets such as equities that have appreciated significantly is to donate the shares to a registered charity. This would result in both a tax credit to the corporation and also contribute to the corporation’s dividend cash account (DCA). Funds from the DCA can be withdrawn tax-free and given to children as a gift, says Rapkin. “Gifting is the tax-free or tax-neutral option.”

For families with multiple properties, giving a child a house or cottage instead of cash can be a wise estate planning choice; however, there could be potential drawbacks. “The best result from an estate planning viewpoint is having nothing in your name when you go,” says Rapkin. “The less you have in your hands on passing, the less probate there will be for the estate. Gifting a cottage to a child during one’s lifetime is considered a deemed disposition at fair market value. The parent would report any capital gain at the time of transfer. This would reduce the future tax exposure to the child. However, with a gratuitous transfer, there is also the issue of land transfer tax, which is based on fair market value.

“Beyond the tax and financial issues, once a property is given away, the parents lose control. If they winter south and then plan to come back in the summer to enjoy the cottage, they may find the child and their spouse have other plans. These kinds of things can turn negative very fast,” says Rapkin.

Helping with a down payment is often only the start of parental financial support. Many young couples find that the ongoing maintenance and tax bills make it hard to keep the property, especially if one partner loses a job. “Parents can plan to address these shortfalls by including certain mechanisms in the Will, such as additional payments for when the child reaches certain milestones like getting married, having a child or at specific ages,” says Rapkin.

Rapkin cautions parents against transferring investments from a holding company to another corporation that buys the home for a child. “When you have a house sitting in a corporation that is really the child’s residence for their personal use, and the child is not paying market rents to live there, you are getting around declaring the money personally to buy the property, but you are losing the principal residence exemption, which still gives the most bang for the buck from a tax perspective. You’re masking the issue and creating a pretty significant tax exposure from a CRA perspective.”

While their hearts may be in the right place when it comes to giving financial gifts to their children, the primary advice is “paper, paper, paper,” says Oxley. “Make sure every detail, every nuance is included. Invest in a good lawyer and make sure everything is explained, and nothing is missed. It doesn’t have to be an intimidating process. It can be a wonderful process when everyone is on the same page.”

Rita Silvan, CIM is a finance journalist specializing in women and investing. She is the former editor-in-chief of ELLE Canada and Golden Girl Finance. Rita produces content for leading financial institutions and wealth advisors and has appeared on BNN Bloomberg, CBC Newsworld, and other media outlets.