Portfolio Confidential - March/April 2026

Why are software stocks down so much? Is this a buying opportunity, or are they heading even lower?

The iShares Expanded Tech-Software Sector ETF (IGV) is down about 15-20% from its 2025 highs, due to intense fear that Artificial Intelligence (AI) will disrupt traditional business models. While the broader market has risen, software stocks are lower as many investors are skeptical that incumbent SaaS (Software-as-a-Service) companies can maintain their high-profit, high-growth, subscription-based models in an AI-driven, usage-based world. There are other factors, too.

1. The "AI Disruption" Fear (The Primary Cause)

Investors are worried that AI tools will allow businesses to build their own custom software, rendering traditional software subscriptions (like Salesforce or Adobe) obsolete or redundant, or at the very least, slowing growth in SaaS revenues.

- In-House Development: Customers are exploring using Large Language Models (LLMs) to create in-house tools, reducing reliance on expensive, third-party enterprise software.

- Agentic AI Threat: The rise of autonomous AI agents capable of performing complex tasks threatens to replace the workflows currently managed by software platforms. These tools are good already and getting better every day. The growth in Clawdbot (a personal agentic tool doing some amazing but possibly unsafe and insecure things) is an example.

- High-Cost Shift: Roughly 70% of software providers indicate that the high cost of computing power (General Processing Units- GPUs) needed for AI features is eating into the profit margins. As a result, they will likely need to move to “consumption-based” pricing models based on token use (tokenomics). Buyers of enterprise software may be uncomfortable with that kind of variable pricing.

2. "Good" Earnings Are Not Good Enough

Software companies are still growing, but they are not growing fast enough to justify their previous high valuations. For a decade now, SaaS companies have been among the most highly valued tech companies out there, and the recent correction may just be a reversion to the mean.

3. Valuation Multiple Compression

Software stocks have been "revalued" by the market. Investors are no longer willing to pay high price-to-earnings (P/E) or price-to-sales (P/S) ratios for companies whose future is uncertain; SaaS companies have traded at very high multiples for years.

4. Increased Competition

The competition is coming from not only companies using AI coding tools and agentic to replace part of the SaaS “stack” internally, but also from new entrants. It’s also a lot easier to create a new SaaS company using these tools.

5. Private Equity Overhang

Many tech-oriented PE companies backed up the truck on SaaS companies around 2018-2022. They overpaid for many of them, and with no real IPO window, and strategic buyers refusing to pay hefty multiples anymore (see above for valuation compression), the PE firms are stuck. They want to sell at least some of their SaaS investments, and they are under pressure from unitholders to provide liquidity, so they are (in some cases) selling at a discount, driving software (especially SaaS) down even further.

Buy, Sell or Hold?

There are defenders of SaaS who say the correction has gone too far and it’s time to buy. Others point out that big companies like SAP or Salesforce are not “point solutions”, but massive ecosystems. It might be easy to use agentic AI to replace a single function but replacing that whole ecosystem (especially with things like regulatory and governance compliance) is not possible with AI—at least not yet.

Would I double down on software stocks today?

There’s an old trader’s maxim: don’t fight the tape. I could be wrong, but this AI overhang feels like it’s going to get worse before it gets better.

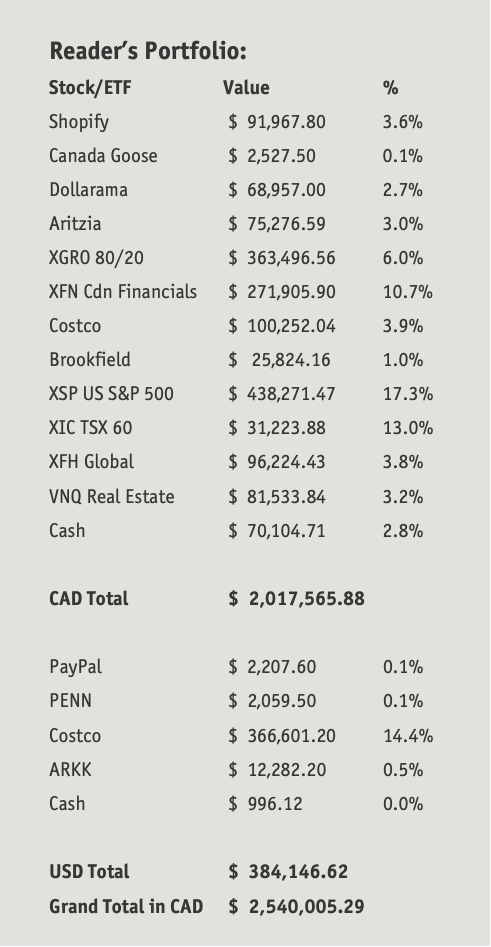

My wife and I are in our mid-50s, and I manage our combined portfolio of two Registered Retirement Savings Plan (RRSP) accounts. I don’t think we will need to start drawing any income until we are required to do so, and our goal is to maximize growth for the next 15 years plus. My holdings are a bit of an eclectic mix—some of the stocks I haven’t bothered to sell as they are very small positions. I have a deep personal understanding of one of the businesses that makes up a larger portion of our portfolio. I’m interested in your thoughts.

When I talk with readers on our 30-minute confidential Zoom calls, the first thing I try to do is investigate whether they have thought about (or ideally written about) all the inputs that go into an Investment Policy Statement. An Investment Policy Statement (IPS) is a highly customized, written document defining an investor's objectives, risk tolerance, time horizon, liquidity needs, legal requirements, tax liabilities and unique preferences. This document acts as a “voice of reason” that encourages ongoing alignment between long-term goals and investment strategy, intended to protect against emotional, impulsive decisions.

The second thing I do is to spend time discussing an investor’s unique preferences. Do they have any specific restrictions, such as avoiding certain companies (e.g., due to bad experiences) or adhering to religious or ethical guidelines? In some cases, the unique preferences are for companies they have fallen in love with for whatever reason, and this has led to an overweighting of the stock(s) relative to their overall portfolio.

Regarding this reader’s portfolio, it is more or less aligned with his and his wife’s objectives for long-term growth (thus the equity orientation). From a risk management perspective, his unique preferences have the potential to undermine his progress. Although he feels strongly that his personal favourite will outperform, what happens if it doesn’t? One of the most common mistakes investors make is falling in love with a stock and having a disproportionate amount of money in their beloved. And one of the most common rationales for doing so is “I have special insights into this company!”

I’d prefer to see a more disciplined approach that doesn’t rely on emotional attachments at all. Here we have 9 stocks, and I recommend rebalancing to equal weights. For the sake of risk management, try to love them all equally! Since three of the stocks currently have only a 0.1% weighting in the portfolio, I would either get rid of them entirely or include them as core holdings with equal weightings.

Idea: If you just can’t bear to sell, move your overweight position to a separate account and label it “speculative”—look at this as a standalone holding that could win big or lose big. This way, you will no longer be skewing the performance return or strategy of your “normal” investment portfolio.

On another note, I’m not clear about the strategy around holding six different Exchange-Traded Funds (ETFs) or the percentage invested in each of them. Also, some of them aren’t particularly great performers. For example, iShares Core Growth ETF (XGRO) is a fund of funds that targets a global strategic asset allocation of 80% equities and 20% fixed income. It invests in eight different ETFs with a 74% total exposure to North America. The Management Expense Ratio (MER) is 0.17%, and the average return from inception (1 January 2008) is only 5.76%.

Another example is iShares Core S&P 500 Index ETF (CAD-Hedged) (XSP), which replicates the performance of the S&P 500 hedged into Canadian dollars. The MER is 0.08%, and the average return from inception (1 January 2002) is 6.46%. How does that return compare to the benchmark? AI tells us that “An investment of $100 in the S&P 500 on 1 January 2002 would have grown to approximately $934.23 CAD by the end of 2025 (assuming reinvested dividends). This represents a total return of over 834%, or an average annual return of 9.76%.”

As a reminder, in his 2013 letter to Berkshire shareholders, Warren Buffett shared the directives he has included in his Will: “One bequest provides that cash will be delivered to a trustee for my wife’s benefit…my advice to the trustee could not be simpler. Put 10% of the cash in short-term government bonds and 90% in a very low-cost S&P 500 index fund.”

A simple strategy is often the best way to achieve growth over time.