In Defense of Cash

Most investors intuitively recognize the benefit of purchasing distressed assets “on-sale” when markets periodically correct, yet very few actually hold the cash required to take advantage of these fire-sale prices when significant market draw-downs inevitably occur. There are few better examples of this type of destructive behavior than the February 2020 stock market panic which found overconfident equity investors near-fully allocated to stocks just prior to the crash. With interest rates sitting at some of their lowest levels immediately preceding the market sell-off, real returns on cash had all but turned negative as supposedly “safe” savings were gradually eroded through the hidden tax of inflation. Far from serving its traditional role as the premier form of liquidity among increasingly yield-starved investors, cash had simply become a toxic asset to be avoided at all costs.

Most investors intuitively recognize the benefit of purchasing distressed assets “on-sale” when markets periodically correct, yet very few actually hold the cash required to take advantage of these fire-sale prices when significant market draw-downs inevitably occur. There are few better examples of this type of destructive behavior than the February 2020 stock market panic which found overconfident equity investors near-fully allocated to stocks just prior to the crash. With interest rates sitting at some of their lowest levels immediately preceding the market sell-off, real returns on cash had all but turned negative as supposedly “safe” savings were gradually eroded through the hidden tax of inflation. Far from serving its traditional role as the premier form of liquidity among increasingly yield-starved investors, cash had simply become a toxic asset to be avoided at all costs.

This aversion to cash was further compounded by the fact that most investors have been conditioned to believe that virtually any allocation to “idle” cash which is not “put to work” in the stock market merely serves as an unnecessary opportunity cost on long-run portfolio performance. Instead, investors today largely adhere to a strategy whereby they simply rebalance between different risk assets on a regular basis to maintain their original asset allocations. For example, if stocks were to fall relative to bonds, an investor with a target weighting of 60 percent stocks and 40 percent bonds would re-balance their portfolio according to pre-defined rules by selling bonds and purchasing stocks in order to re-establish their original 60/40 allocation.

This act of systematic portfolio rebalancing serves to automatically sell high and buy low, which is precisely what bargain-seeking investors ought to be doing, at least in theory. The problem with this line of reasoning is that there are occasionally periods when all asset markets become over-valued simultaneously and subsequently incur large-scale draw-downs in unison. Indeed, at one point during the late-February market sell-off, long term US Treasury Bonds were down over 20%. In other words, those bonds that you were relying on to sell “high” in order to buy depressed stocks might themselves be grossly underwater at the exact moment you need them the most. Bonds might not be down quite to the same degree as stocks, of course, but selling one depressed asset to buy a slightly more depressed asset strikes us as little more than simply re-arranging deck chairs on the Titanic.

The truth is that investors largely fail to appreciate the fact that asset correlations tend to be dynamic throughout history. The long-run 100-year or 50-year correlations that investors often rely upon can, and do, break down for entire decades at a time. Negative correlations can suddenly turn positive, which should be all the evidence investors need to realize that simply holding a historically uncorrelated basket of risk assets is hardly a substitute for near-term liquidity. Unlike stocks, bonds, commodities, or real estate, only cash grants investors the unencumbered right to purchase distressed assets at the precise moment when prices are the lowest and expected future returns are the highest. Whereas stocks and bonds are effectively just claims on variable quantities of future liquidity, cash is immediate liquidity in and of itself.

It is true, of course, that once inflation is considered, holders of cash face the non-trivial possibility of incurring real losses over the years ahead. But investors often forget that these losses will be realized in a slow and predictable manner, whereas virtually all other asset classes have the potential to incur losses in a decidedly unpredictable and volatile way. It is precisely this stability in the face of relative market volatility that gives cash its true underlying value. This, of course, is the often-unheralded value of optionality.

One of the more coherent frameworks for thinking about this embedded optionality comes from none other than Warren Buffett, who has a rather interesting way of thinking about the true value inherent in cash1. He considers holding cash to be akin to holding a call option on every single asset class with no strike price or expiration date. The cost of holding this option—the option premium if you will—is merely the opportunity cost of holding a low-yielding asset like cash relative to other potentially higher returning risk assets. When he feels this premium is cheap (ie. the opportunity cost of holding cash is low due to the high price of competing alternatives), he becomes comfortable holding large allocations of cash for extended periods of time.

Critics will be keen to dismiss this argument by pointing out that once the potential for high inflation is taken into consideration, cash is hardly the oasis of safe liquid purchasing power its proponents like to claim. As the argument goes, double-digit inflation can quickly erode the value of cash and encumber an investor’s ability to purchase depressed assets just the same as any market draw-down ever could. While this belief has certainly gained widespread acceptance among the majority of investors today, it is also largely false. The narrative that high inflation destroys cash returns is an all-too prevalent myth that has been widely propagated by an investment industry seeking to scare investors out of cash and into the arms of managed money.

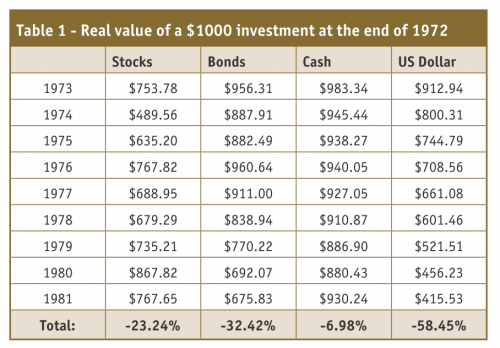

As can be easily seen through even a cursory examination of the inflationary 1970s and early 1980s, the historical record clearly shows that cash tends to perform relatively well during periods of high inflation. As Table 1 illustrates, 1973-1981 was a period during which the dollar lost a cumulative 58% of its total value, and yet a $1000 investment in cash at the beginning of 1973 yielded a real loss of only -0.8% per year by the end of 1981. Indeed, after accounting for inflation, an investment in cash incurred a total real loss of only 7% over the entire nine-year period, versus much heavier losses of approximately 23% for stocks and 32% for bonds.

Investors are often left incredulous at the fact that cash was largely able to maintain its purchasing power throughout the 1970s against the backdrop of widespread dollar devaluation. The reason for this lies in the fact that during periods of high monetary devaluation when inflation tends to move sharply higher, short term interest rates increase rapidly as well. While investments with fixed payouts such as bonds suffer large losses as their income distributions are greatly eroded by inflation, cash investments benefit from the rapid upwards adjustment of interest payments on short term savings.

While inflation may have indeed reached double digits in the late 1970s, so too did rates on short-term cash accounts. As a result, cash, rather counter-intuitively, served as one of the few reliable inflation hedges of the 1970s. This, of course, runs counter to the popular narrative that it is stocks which serve as the premier inflation hedge, whereas cash should be unequivocally avoided during times of rising inflation. While many investors still adhere to this popular myth, the inflationary 1970s provide the perfect counter-point illustrating the superiority of cash versus equities in a high-inflation environment.

It turns out, then, that cash uniquely provides its holders with the unassailable option to purchase fire-sale assets in down markets, irrespective of inflation. Of course, we can already hear the chorus of protests proclaiming that cash’s much-touted optionality is nothing more than an ill-disguised attempt at market-timing. But what these critics would call “market-timing”, others would simply call intelligent asset allocation reflecting the real-world risk/return relationship between various asset classes. In the lead-up to the global stock market sell-off that began in late February, for example, equity return forecasts were actually projecting negative 10-year nominal returns for large-cap US stocks2, whereas cash was likely to accrue at least some small positive nominal return to investors over this same period.

But all of this begs the question: if cash was a non-volatile asset that had the potential to deliver an annual return of approximately zero over the next 10 years, yet stocks were highly volatile and projected to have negative annual returns over this same period, surely a rational investor would have logically sought to optimize risk-adjusted returns and allocate a far larger portion of their holdings to cash than they actually did. This doesn’t mean that investors should have sold all their stocks prior to the February market panic and allocated 100% of their holdings to cash. What it does mean is that if cash had a high probability of commanding a superior risk/return profile relative to stocks over the next 10 years, holding at least a portion of your portfolio in cash would seem be an entirely sensible proposition.

Of course, forecasts are just forecasts, and rather than going into free-fall in late February, stocks may have very well gone on to deliver a solid string of uninterrupted positive returns had the COVID-19 pandemic never occurred. But with equity prices hovering at such elevated levels just prior to the late February market sell-off, the opportunity cost of holding cash at the time would seem to have been uncharacteristically low. In other words, using Warren Buffett’s cash optionality framework, maybe the “option premium” investors were paying to sit in cash just prior to the stock market panic was historically quite cheap - perhaps even approaching zero. In such an environment, where it essentially costs nothing for investors to reject market risk, holding even just a small portion of one’s portfolio in cash would seem to be not only defensible, but actually quite prudent.

Brian Chang is the author of the finance blog Crusoe Economics (https://crusoeeconomics.com). He resides in Vancouver and can be contacted by email at info@crusoeeconomics.com or on twitter @CrusoeEconomics.