Saving Strategies You Can't Afford To Ignore (Over $110,800 In Savings!)

While it’s always pleasant to save a few bucks during a sale or find a great deal on that item you’ve been craving, most, if not all of these savings pale in comparison to the amount of money you can save and receive for free when it comes to investing.

While it’s always pleasant to save a few bucks during a sale or find a great deal on that item you’ve been craving, most, if not all of these savings pale in comparison to the amount of money you can save and receive for free when it comes to investing.

Sure, $50 off a new phone might sound great, but what about a free $7,200 that you can receive right from the government? Not good enough? How about receiving a guaranteed 100% return on your money, coming directly from your employer?

Yes, I admit, when put that way it sounds too good to be true, but these are all legitimate benefits that the Canadian government and our employers want us to take advantage of!

So, do you want to spend your free time finding out how to save a few bucks on your next shopping excursion, or would you rather take advantage of some of these strategies and programs that can increase your net worth by the thousands (even hundreds of thousands in many cases)?

Here are some of my favourite strategies that can set you up for success when it comes to you and your family’s financial wellbeing and net worth:

The Easiest Way To Save $100,000

Not only does Canada have some of the highest mutual fund fees in the world (which can cost you hundreds of thousands of dollars over your lifetime), but it also has the distinction of being the world leader in closet indexing. What does this mean?

Closet indexing refers to mutual funds that you may be holding which were marketed to you as actively managed funds that will ‘hopefully’ beat the market, when in reality, they simply hold the market. The catch is that you can own the market yourself without them while paying a small fraction of what they are charging you (over 40 times cheaper is not uncommon).

To put that in perspective, imagine paying 40 times more for a car, a house, or a TV. That would be unheard of in other industries. Yet, when it comes to the investment industry, this is a common occurrence that’s easy to miss and can be the key factor that will enable you to retire years earlier.

Let’s use some real numbers to help illustrate the point:

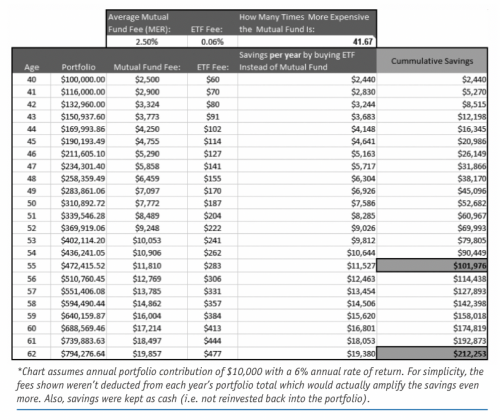

A typical mutual fund in Canada charges around 2.50% (this fee is referred to as the Management Expense Ratio (MER)). That’s a fee of $2,500 per year on a $100,000 portfolio. This fee is automatically deducted from the investments, so you never see the money physically leave your account which makes it so easy to miss.

Compare this to an Exchange-Traded Fund (ETF) that you can buy yourself which holds the Canadian market. For example, one such iShares Core S&P/TSX Capped Composite Index ETF (XIC) which has an MER of 0.06%. On that same $100,000, your fee would only be $60. In other words, with the mutual fund, you are paying $2,500 per year in fees instead of $60.

That’s a savings of $2,440 EVERY YEAR on that $100,000 portfolio. Keep in mind, too, that this $2,440 saved now automatically stays invested to further grow your portfolio and provide you with extra dividends.

In other words, this $2,440 continues to compound and grow, which never would have happened if it was given away as fees in the mutual fund.

How would you like to save $2,440 by making such a switch?

Keep in mind, too, that as your portfolio grows, the amount saved continues to get bigger, and the savings continue to compound. Over time, the savings can easily reach $100,000+ as shown in the table below:

As you can see, by age 55, the amount of fees saved has reached $101,976. By age 62, the amount saved has climbed to $212,253.

What if your mutual fund isn’t doing closet indexing? Well, even if your mutual fund isn’t closet indexing, it is extremely difficult for any mutual fund to beat the market after including the high fees they charge.

How difficult? According to SPIVA® , 92% of actively managed funds underperformed the index over the last 10-year period in Canada. Since a mutual fund’s past performance is no indication of future results, how can you be sure that you have the skill to somehow be able to predict the top 8% of mutual funds every year? The best minds in the industry aren’t able to pick the best mutual funds consistently, so what chance do you and I have?

At a typical MER of 2.5%, that means the mutual fund must beat the market by 2.5% every year just to break even. That’s a tall order, and the data proves it with 92% of mutual funds failing to beat the market. It’s also worth noting that you pay this fee even if the mutual fund loses money. Why would you take on the risk of an extra 2.5% fee which you have to pay regardless of how the fund does, when the chances of the mutual fund beating the market are so slim?

While purchasing ETFs can be a great solution, the next question becomes “What are the top ETFs to consider?” and “Is there a way to bypass the fees entirely?”

At 5i Research, we’ve answered thousands of questions about the top ETFs in Canada, and as a member you can view all past answers, as well as ask your own to the 5i Research team.

Can you avoid fees entirely? Definitely. By buying stock directly, you bypass the fees that ETFs and mutual funds charge. While ETFs can be a great way to build a great low cost and diversified portfolio, another option is to eliminate those fees completely by creating your portfolio using one of 5i’s 3 model portfolios. Our balanced portfolio, for example, has had an annualized return of 20.7% per year since inception. You can view it, as well as ask the 5i Research team your investing questions by trying out the membership risk-free for 60 days by going to www.canadianmoneysaver.ca/trial

A Guaranteed 100% Return On Your Money?

If anybody tells me that they can get me a 100% return on my money, I tend to run for the hills. “Too good to be true,” I say. “Nobody can guarantee returns that high!”.

Yet there is one exception: Have you taken full advantage of the Registered Retirement Savings Plan (RRSP) company match that your employer offers?

Many employers will match your RRSP contributions up to a certain limit every year. If you haven’t done so, ask your company’s Human Resources (HR) department about this now. It is literally free money; if, for example, you put in $1,000, the company will add another $1,000 to your account!

That’s a guaranteed 100% return on your money!

Even if they only match 80%, that’s still an 80% return on your money. Nowhere else can you get a guaranteed return that high.

The numbers vary from company to company so make sure to read the details in terms of the maximum allowable contribution per year, how much they match, and what the process is to receive the free funds. Nowhere else is there a guaranteed way to double your money like this, and the quicker you do this, the quicker your money and your employer’s contribution can start growing and compounding for you.

This isn’t one of those “We’ll get to it eventually” moments. It’s something you must act on now so you won’t lose your free company match for the year!

How much are you missing out on if you don’t do this? Employers typically match between 3% to 6% of your salary. At a salary of $60,000, that’s between a free $1,800 to $3,600 per year!

A Free $7,200 From The Government?

Did you know that you can receive $7,200 for free, for every child that you send to post-secondary education? Not only that, but the growth that you generate on that amount (plus your own contributions) will grow tax free until you are ready to take it out.

As an added bonus, when it finally does start to be withdrawn, it will be under your child’s income and not your own, meaning that the tax payable will be in the lowest tax bracket. How’s that for a good deal?

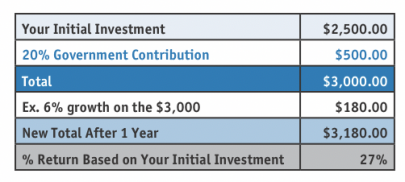

With a Registered Education Savings Plan (RESP), this is exactly what happens. Every year, the government will take what you contribute, and give you a free 20%, up to a maximum of a free $500 dollars per year! Do this for the years leading up to your child going for a post-secondary education, and you can receive up to $7,200 per child.

In other words, it’s like receiving a guaranteed 20% return on your money every year (i.e. If you put in $2,500 per year, you’ll receive a free $500 for that year). No stock, bond or Guaranteed Investment Certificate (GIC) is ever going to guarantee you a 20% return, making this a no-brainer.

Keep in mind, too, that over time, that free $500 is invested and continues to grow along with your contributions. Therefore, if we estimate a reasonable return of 6% per year on those investments, then over the course of one year, you would have received a “conservative” projected return of 27.2% ($3,180/$2,500). Now you’re actually earning a higher return than what credit cards charge! Not bad.

Too Busy for an Extra $100,000+?

I hope that you have found these money saving (and earning) strategies useful. It’s easy to get distracted by shopping for “hot sales” where we can save a nice $20 or even $50 on some consumer item that we may not even need. Or spending hours doing comparison shopping to save the $50-$100 on some new furniture, appliance, or electronic item. While these is nothing wrong with saving money in this way (heck, I do it too), remember to not miss the forest for the trees, and instead prioritize items like the ones mentioned here to add tens of thousands to your net worth, instead of a mere $50-$100.

In the investing space there is lots of easy low-hanging fruit like the strategies mentioned above, where with a bit of research and effort, your savings and earnings can be in the thousands (even hundreds of thousands as is the case when comparing low cost Do-it-Yourself investing to high-fee mutual funds).

Have questions about some of these strategies, or particular stocks or ETFs that you’re considering? Try 5i Research risk-free for 60 days to see all our past answers on these topics, along with the ability to ask our Research Team all your investing and personal finance questions.

The team does not sell ANY investments and does not take ANY payments from any companies that do sell investments. This makes their answers truly conflict-free, keeping your best interests at heart. We hope you give us a try and let us be your truly unbiased source for your investing questions.

You can try 5i risk-free for 60 days by going to www.canadianmoneysaver.ca/trial

Kornel Szrejber, BBA, is a Contributing Editor at Canadian MoneySaver. kornel@5iresearch.ca