2026 Outlook: Will A Banner 2025 Leave Investors Flapping In The Wind?

The years seem to go by faster every year, and once again, it is hard to believe that we are starting a brand-new year, with 2025 now in the rear-view mirror. While 2025 started a bit bumpy with tariff drama in the first quarter of the year, most Canadians are hopefully content with how the year progressed, at least from an investment perspective. To take stock of what 2026 might hold, we need to take a bit of inventory of where things stand and how the prior year progressed.

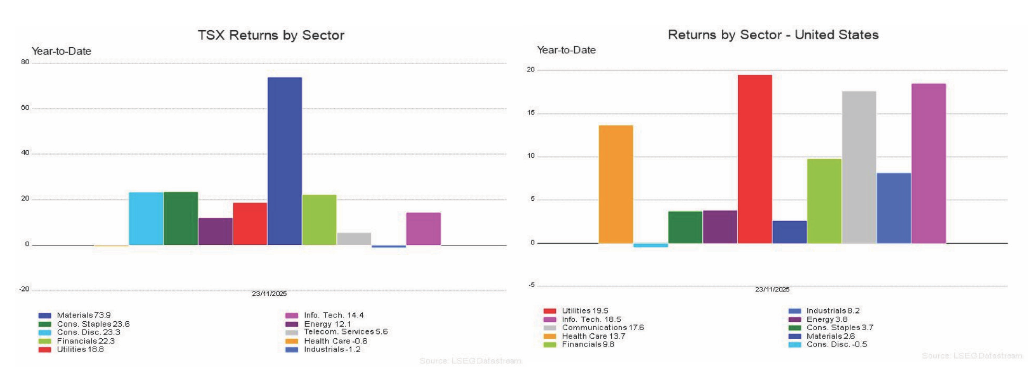

With an initial decline at a trough of -9.6% for the TSX in early April 2025, the index later rallied to an impressive 22.7% as of 24 November 2025. A lot of this was due to a very strong Materials sector, but Financials also did some heavy lifting this year, which is nice to see.

On the U.S. side, markets saw an initial dip in the early part of 2025, but a strong remainder up until November, where there was a bit of a mini-meltdown across stocks, driven by Artificial Intelligence (AI) fears. While the S&P 500 is still managing to have a decent year, up 14.2%, the turmoil underneath is seen through the equal weight index (represented by the Invesco S&P 500 Equal Weight Exchange-Traded Fund (RSP)) that is “only” up 6.8% as of 24 November 2025.

Going by sector, as of 23 November 2025, here is what returns looked like in the U.S. and Canada. While sector performance in the U.S. was a bit more variable, Canada had quite a strong showing across sectors, with Materials as the obvious standout. The performance in Materials, a sector that had lagged for some time, is a great example of why diversification in a portfolio is so important.

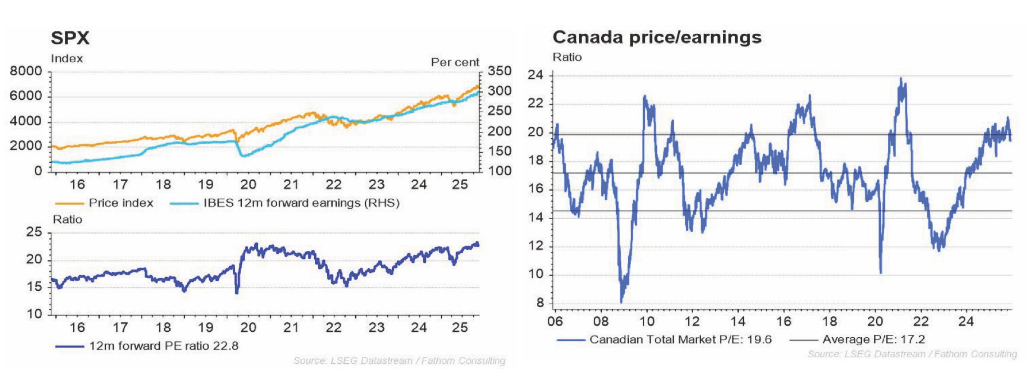

As we head into 2026, here is where the TSX and S&P 500 sit from a valuation perspective, and where valuations have been in the past. We see two primary takeaways here. The first is that both the TSX and S&P 500 are flirting with highs in their valuations. The second is that while on an absolute basis the TSX is cheaper than the SPX, the TSX has traded in a well-defined range over the years and is at the high end of that range currently.

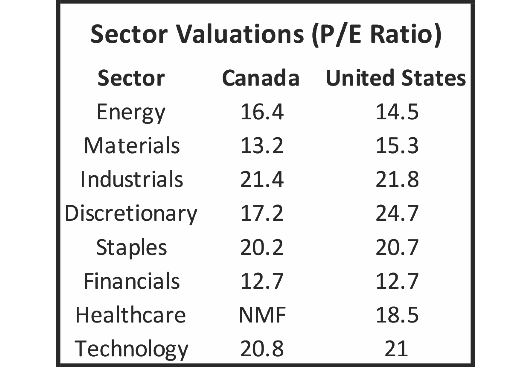

Here is a bit more granular sector valuation in Canada and the U.S.

Source: LSEG

One other important piece that feeds into valuation is what earnings growth looks like. S&P Global estimates that the S&P 500 is going to see earnings grow by 16% in 2026. This compares to National Bank estimates for the TSX at 11%, much of which is being driven by the Materials and Real Estate sectors, per their estimates.

On the macro side, we think this is where things between the U.S. and Canada will diverge a bit. While Canada is home to great companies, the Canadian economy appears to have a bit of an anchor weighing these down. Tariffs, while out of our control to some degree, are not going to help growth. Meanwhile, the Real Estate sector seems to be treading water, and finally, a pullback in immigration will also lead to slower nominal growth. Without allowing Materials and development related to the Material/Energy sector to really flourish, we find it hard to paint a picture where Canada is able to find a driver for economic growth in the near term. Now, in fairness, we probably would have had the same thoughts last year, and the TSX has had a banner year for performance. A great reminder that the stock market is not the economy, even if many TSX constituents are more anchored to broad economic growth! While the Materials sector was a big contributor to the TSX this past year, the nature of commodities markets means that there is likely some short-term ceiling to the run that metals have had. The Canadian banks have done well over the last year, but we would not bet on them pulling another rabbit out of the hat like last year, as one way or another, they will be tied to the broad Canadian economy. This, of course, does not mean they won’t do “fine”, we just might not expect a 20% run from the banks. Where Canada might see an unexpected bright spot is if the federal government can quickly and aggressively execute on some of its investment plans for major projects and defence.

On the U.S. side, the macro landscape looks a bit more constructive. While things are slowing down, certainly, they don’t have the same anchors weighing down growth (tariffs) to the same degree as Canada (since it is the U.S. imposing these tariffs). The U.S. also has leaned into the AI infrastructure buildout, which will help support the economy regardless of consumer issues in the short-term, something that, for whatever reason, Canada appears to have missed the boat on for now.

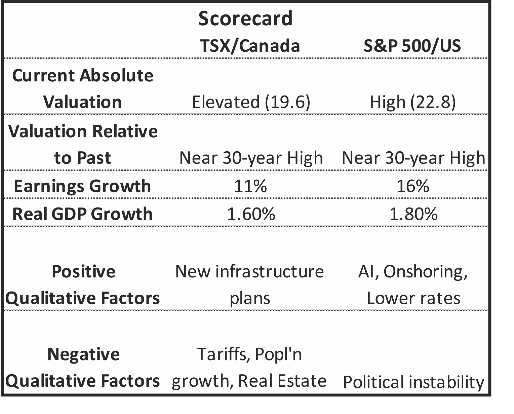

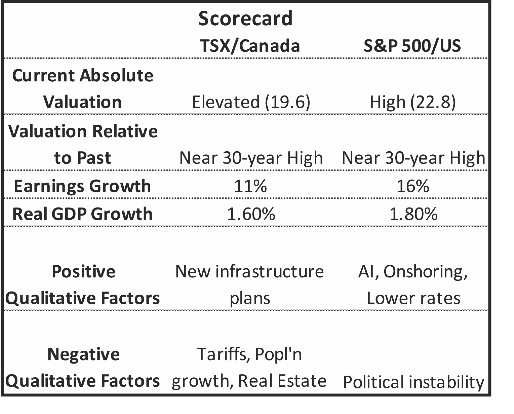

A picture (or table) is always worth a thousand words, so let’s look at a bit of a scorecard to take stock of all these factors. You can have an expensive market but justified by lots of “good stuff” happening, or have a cheap market but with few prospects, or some mix of scenarios in between. In turn, we need a way to account for a bit of everything:

While the above might not be an all-encompassing list of things that will impact markets next year, it gives us a high-level view of the situation. The broad large-cap indices in Canada, while not at concerning levels, we think will have their work cut out for them. They are trading around past highs, albeit with some justification, but economic growth is starting to take a breather in North America. While the SPX is at a high historical valuation, earnings growth does give some credence to this number. The TSX is maybe standing on shakier ground, not to mention that earnings growth from Materials companies is likely to be a bit more fleeting than other sectors. Meanwhile, Canada has fewer positive qualitative factors that we think an investor can point to and a few more negative qualitative factors, but nothing we would view as particularly “concerning” longer-term.

We think this is an interesting, if not nuanced, setup for the TSX in 2026. On one hand, there is no clear and present danger that we see in terms of a “Bear case” to be made. On the other hand, there also isn’t much we see to be particularly enthusiastic about, either. The upshot of this is that markets can do just fine in this type of scenario. Sometimes the absence of bad news is, in itself, good news!

On the U.S. side, we think there are a few more “catalysts” to provide a positive narrative between onshoring efforts and AI, which can be a double-edged sword if, or when, that investment spigot is shut off. Meanwhile, like Canada, we don’t think there is an obvious risk facing the markets in 2026 at this stage. The political landscape has certainly tried to throw curveballs in 2025, and more may come next year, but given how the last few years have played out, a quiet year on the news and geopolitical front might be all that markets need to have an adequate year.

Overall, we think an investor should set expectations for more of an average year in the markets, closer to a 5% or 7% return, which is still healthy. While we can always hope for another double-digit year, we might temper our expectations for mainstream North American markets, as the TSX has had a bit of an outlier year, and the S&P 500 might need to digest the last few years of strong returns while it sits at high valuations as well. The TSX has only seen seven instances of back-to-back double-digit return years over the last 40 years, many of which tended to follow larger market drawdowns.

2026 might be a year where a few themes work out well, while the broader markets struggle to find their footing. This is due to the setup for valuation and broader economic growth in North America. On the Canadian side, never say never, but it is hard to see another 20% year in Financials, let alone 70%+(!) in Materials. On the U.S. side, while betting against the Mega-Caps has almost always been a losing bet, as these companies invest heavily in capital expenditures to fund the AI Infrastructure buildout, 2026 might be the actual year that the Mega-Caps lag, as investors question the returns from the AI investments they are making.

If that is the case, then what are the key themes for 2026?

We think there are a few areas for an investor to focus on:

Don’t Call it a Comeback – The AI Trade

A lot of pearl-clutching has occurred over the last few months about whether AI is in a bubble, and ironically, all this fear has made it even more unlikely that we are in any sort of bubble. In fact, the recent drawdown in a lot of AI-related companies has created an interesting opportunity for investors to reconsider an investment, as valuations have compressed, while nearly every company we could see has reported earnings with commentary to the effect of demand far outpacing supply, and increasing investment into AI.

All the scrutiny and fear around the AI thesis has created an interesting opportunity, and we view the AI theme, which was a driver of returns in 2025, as having the potential to be a driver in 2026, as well.

Don’t Fear Your Robot Overlords… Yet – Robotics

We think markets are overlooking the rise of robotics. The idea of a robot in your home might seem like a fantasy from The Jetsons cartoon, and while it still might be years away, we think this reality is coming a lot sooner than many expect. What is the reason this is coming sooner? First, technological advancements tend to come quicker and quicker. Just think about how ChatGPT came onto the scene. AI has been a “thing” for some time but was usually referred to as Machine Learning and was “just” something that was running in the background of technology-focused institutions, making them operate more efficiently. Then ChatGPT launched and essentially changed the narrative across the labour market, economy, business landscape and, well, almost everything really. It proliferated and started changing businesses in months, if not weeks.

We see robotics as having a similar type of lightbulb moment, and we think it is closer than most expect. Now, in fairness, not everyone is going to have a robot folding their laundry within weeks of some technological breakthrough, but the speed at which companies will invest and iterate into this technology will be at a breakneck speed. We expect the cadence for robotics to be similar to AI. Something that everyone knows is “out there”, but once the jump happens, it will happen very quickly.

The other reason we see a robotics revolution as being closer than many think is, ironically, because of AI. Advancements from AI, as well as the step change in computing power, have more than likely pulled robotics ahead by years. Now, robots have more ways that they can interact and utilize “logic” with their environment, and also have vast computational resources to help support their proliferation. AI and the infrastructure buildout are enabling the use cases for robots. Once again, while we might not have robot butlers in our houses in 2026, from an investment perspective, we think there is going to be an increasing level of investment and interest in this space.

The Old Faithful Staples: Consumer Staples

You cannot say that we aren’t flexible in seeking out opportunities, as Consumer Staples could probably not be more different from the above two areas to focus on! The Staples sector is a bit thinner in Canada compared to the U.S., so this likely applies a bit more to the U.S. side of things, but regardless, we see Consumer Staples as starting to show an interesting risk-reward opportunity.

Over the last few years, many of these companies pushed price increases a bit too hard, and now that lever for growth is no longer available, as consumers don’t have the capacity to “eat” further price increases. Meanwhile, consumers are also starting to baulk and find alternatives where they can. Add in some changing consumer tastes/trends, and it is easy to see how the Consumer Staples companies got themselves into this situation.

The flipside of this, however, is that many Consumer Staples companies are now trading at mid-teen to even single-digit P/E ratios with dividend yields in the 3% to 5% range. If these companies can hold prices, buy back 2% to 3% of shares and pay a 5% dividend, you quickly get to a healthy 7% to 8%+ return with mitigated downside risk, given the valuation and nature of these businesses. In other words, they are showing a compelling risk/return trade-off, particularly in the context of a broader market that is more expensive. The main risk with Consumer Staples at this stage, we think, is timeframes. While they look interesting for 2026, it might take more than 12 months for markets to really start caring about them, but in the meantime, the higher yields don’t hurt!

If you're still with us, that about sums up our outlook for 2026. If past years have set any precedent, there will likely be some market event by March that blows this outlook (and all others) out of the water, but we can only work with the information we have at the time and that is why investors should always think in terms of years, not a single year, and remain diversified in their approach to investing.

All the best in 2026 and keep moving forward!

Ryan Modesto, CFA

CEO, i2i Capital Management