Where Does Money Come From?

As the generally-accepted medium of exchange, money is unquestionably the most widely traded commodity on earth, comprising exactly one-half of every transaction in a modern economy. Yet, despite its widespread use in economic exchange, very few people have a proper understanding of where modern money actually comes from. Indeed, the majority of people, when asked, claim that it is the government that creates the money we regularly hold in our wallets and see in our bank accounts on a near-daily basis.

As the generally-accepted medium of exchange, money is unquestionably the most widely traded commodity on earth, comprising exactly one-half of every transaction in a modern economy. Yet, despite its widespread use in economic exchange, very few people have a proper understanding of where modern money actually comes from. Indeed, the majority of people, when asked, claim that it is the government that creates the money we regularly hold in our wallets and see in our bank accounts on a near-daily basis.

While it is true that money within the economy takes the physical form of coins in your pocket and dollar bills in your wallet, it more commonly takes the form of a bank deposit in a savings or chequing account at your local bank. The majority of money in a modern economy is in fact held in this fashion—simply as an electronic entry on a ledger with your banking institution. These bank deposits form the majority of a country’s money supply, but it is a mistake to think that the bulk of this money is created by the government. Rather, the vast majority of deposit money is instead created by private commercial banks, who, as part of their regular lending operations simply conjure this money into existence “out of thin air”.

This will undoubtedly come as a shock to many people, for there is a pervasive and long-standing misconception held by both amateur and professional alike that commercial banks merely function as “intermediaries”. This is to say that the majority of people tend to believe that commercial banks accept deposits from the general population and then subsequently, lend these deposits to individuals and businesses seeking access to capital. In reality, under the monetary system of today, when a commercial bank finds a willing and credit-worthy borrower, they provide this borrower with a loan not by transferring over existing savings already held on deposit, but instead by simply conjuring new money into existence with the stroke of a key.

For example, if Bank A agrees to loan Ben $10,000 for five years, it does so by simply creating a new $10,000 deposit in Ben’s account at Bank A. This is not existing money that was simply transferred from Bank A to Ben, but brand-new money that was merely conjured out of thin air. With the new $10,000 in his account, Ben is subsequently free to draw down this $10,000 balance as he wishes either to make investments or purchase various goods and services for consumption. Of course, Ben doesn’t just receive a $10,000 asset as a result of the loan (the money in his account at Bank A). He also takes on a $10,000 liability in the form of a $10,000 debt now owed to Bank A at the end of five years.

And what of Bank A? By creating the $10,000 in deposit money for Ben, Bank A has created a liability for itself in the form of money owed on demand to Ben. This is because Ben’s $10,000 account at Bank A is money payable by Bank A to Ben, due on demand the moment Ben makes a withdrawal. But Bank A does not just obtain a new $10,000 liability as a result of the loan—it also acquires a new asset. This asset is simply Ben’s debt—namely the promise made by Ben to return $10,000 to Bank A at the end of the five-year period. The changes to the balance sheets of both Bank A and Ben as a result of the loan are illustrated in Table 1.

As a result of the loan, therefore, both Ben and Bank A have each acquired a new $10,000 asset and an offsetting $10,000 liability. The financial net worth of both Ben and Bank A has thus been left unchanged, and yet $10,000 of new money was subsequently created out of thin air; it literally did not exist prior to the loan. As Ben spends down his funds, the $10,000 of new money is dispersed throughout the financial system as wages to workers, taxes to fund various government social programs, and profits to businesses. These funds “flow” through the financial system largely as bank deposits transferred back and forth between various commercial banks.

In order to clearly illustrate this process, consider the following example. If Ben pays $10,000 from his account at Bank A to Julian for a service rendered, and Julian deposits these funds into his bank account at Bank B, Ben loses a $10,000 asset and Julian gains a $10,000 asset in return. Bank A has correspondingly lost a $10,000 liability in the sense that it no longer holds the $10,000 deposit for Ben (owed to Ben upon withdrawal), while Bank B has now acquired a new $10,000 liability in the form of the bank deposit now payable on demand to Julian.

Of course, Bank B does not simply accept this new $10,000 liability without receiving an equal asset in return. In order to finalize the transaction, Bank A transfers $10,000 of its “reserves” to Bank B, such that Bank B acquires both a new $10,000 asset (the reserves from Bank A) and $10,000 liability (Julian’s deposit), while Bank A loses both a $10,000 asset (the reserves sent to Bank B) and a $10,000 liability (Ben’s deposit). The balance sheet change resulting from Ben’s payment of $10,000 to Julian is summarized in Table 2. Clearly, as the $10,000 is spent throughout the economy, all that is happening is that existing money is simply moving between different accounts within the financial system, with new money only being created as a result of the initial loan from Bank A to Ben.

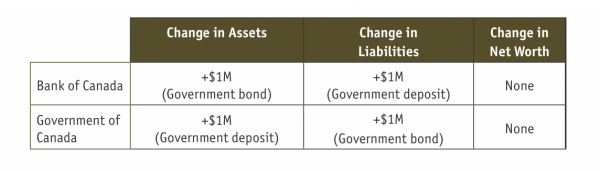

While it is true that most of the money in the economy is predominantly created through private commercial bank lending, money can also be created in a modern economy through another channel—a country’s central bank. The precise legal and technical framework for such an operation differs from country to country, but in Canada this is generally enacted through direct loans to the federal government. When the government issues bonds or treasury bills to borrow funds for spending purposes, the Bank of Canada simply buys these bond/bills and pays for it by conjuring new money into existence.

Specifically, if the Government of Canada wishes to borrow $1M for a five-year period, they simply issue a five-year $1M bond which the Bank of Canada then purchases directly from the government in the primary market. In order to pay for this bond, the Bank of Canada simply adds $1M in new money to the federal government’s account at the Bank of Canada, known as the Consolidated Revenue Fund (CRF). At the end of the transaction, the Bank of Canada has now acquired both a new $1M asset (the bond) and a new $1M liability (the new money in the CRF, now owed on demand to the government). The Government of Canada, similarly, receives an additional $1M in assets (the deposit in its CRF account), while also acquiring a new $1M liability (the money it now owes to the Bank of Canada at the end of five years). Table 3 illustrates the resulting change in balance sheet composition.

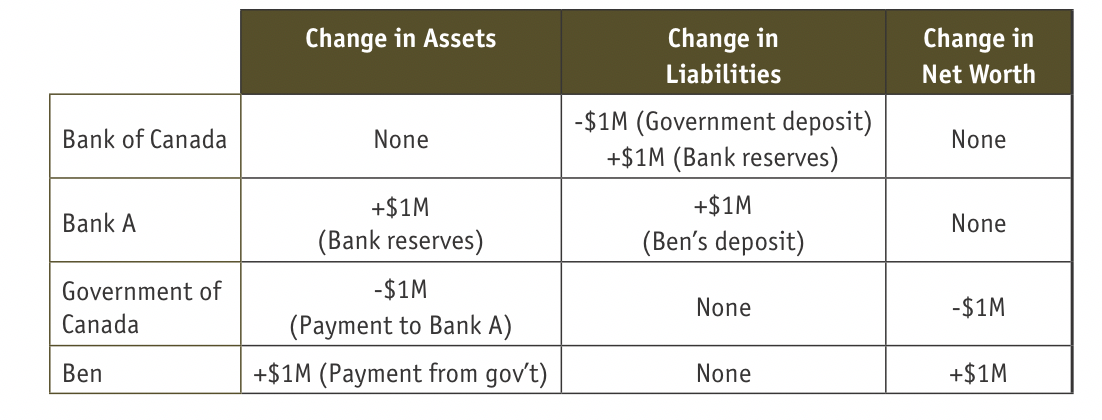

When the government subsequently writes a $1M cheque to Ben, he deposits this cheque in his bank account at Bank A which causes an increase in his deposits by $1M. As was previously explained, because a deposit is a liability of Bank A, normally the sending bank would also transfer $1M of its reserves to the receiving bank (Bank A in this case). However, because the sending bank is, in this case, the Bank of Canada, a slightly different operation is undertaken to offset Bank A’s new liability. Rather than reserves being transferred from the Bank of Canada to Bank A, $1M of government deposits are instead transferred from the CRF to Bank A’s reserve account with the Bank of Canada. The resulting change to the balance sheets of Bank A, the Bank of Canada, the government, and Ben are shown in Table 4.

Thus, subsequent spending by the Government of Canada in the private sector (either for goods and services rendered or outright transfers) has resulted in $1M in new deposit money being created in Ben’s account at Bank A. As Ben spends down these funds on goods and services, the new money “flows” throughout the economy in a similar manner as laid out in Table 2. Government deficit spending, financed directly by the Bank of Canada, has therefore created $1M of new money for the private sector1.

We can see, then, that in a modern economy money is created primarily through commercial bank lending and secondarily, through Bank of Canada loans directly to the government. While money-creation by the Bank of Canada tends to be deliberate and calculated, money-creation by private banks is much more dependent on the current state of the economy. Since it is the establishment of new bank loans that create most of money, the overall money stock is predominantly determined by the willingness of both commercial banks to make loans and the private sector to take on debt. Understandably, such willingness to both borrow and lend tends to fluctuate significantly alongside the cyclical nature of a modern economic society.

Brian Chang is the author of the finance blog Crusoe Economics (https://crusoeeconomics.com). He resides in Vancouver and can be contacted by email at info@crusoeeconomics.com or on twitter @CrusoeEconomics.

1. It is noteworthy that the above method of money-creation applies only to loans made by the Bank of Canada directly to the government. While not true for all central banks, Bank of Canada purchases of pre-existing government bonds from investors in the secondary market does not actually create new money.