Seasonal Reasons For A Bullish Spring

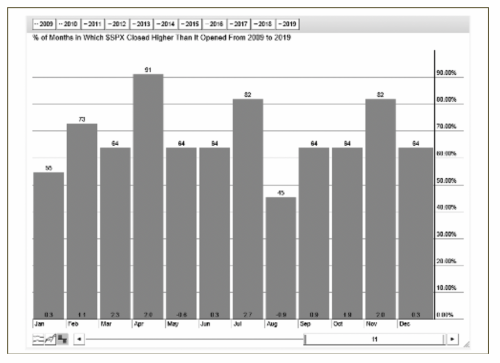

Above is a month-by-month seasonal chart for the S&P 500 from 2009 to the end of 2019. The chart shows us how often the SPX has a positive return in each month over that 11-year history. If you go back further, much of the same pattern exists with a few variations. One consistent seems to be the period between February and May. In April, the SPX has made positive returns very consistently (91% of the time!). This tendency has been seen on longer termed horizons as well.

Above is a month-by-month seasonal chart for the S&P 500 from 2009 to the end of 2019. The chart shows us how often the SPX has a positive return in each month over that 11-year history. If you go back further, much of the same pattern exists with a few variations. One consistent seems to be the period between February and May. In April, the SPX has made positive returns very consistently (91% of the time!). This tendency has been seen on longer termed horizons as well.

Technical Reasons For A Strong Market Until The Spring

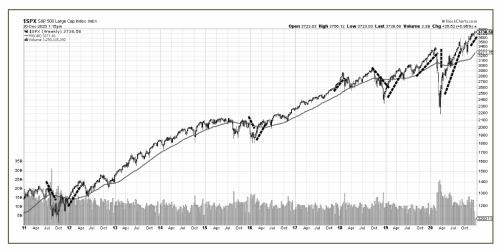

Readers might be interested in knowing that I’m working on my new book on contrarian investment strategies – I hope to see it released by the spring. One of the more basic indicators I am covering is the angle of ascent or decline of a recent move when compared to the historic angles. A steeper than normal angle of ascent is much like any sentiment indicator, in that it can signal irrational exuberance by the crowd. Since March of 2021, we have a parabolic looking chart on the S&P 500. The chart below illustrates this extreme angle of ascent. Markets tend to regress a bit when investors find even the smallest reason to take profits after such a move. I’ve marked some of these sharper than normal moves (up or down) on the chart with small black trendlines. Note the resulting reversals (pullbacks) that the S&P 500 experienced after the angle of ascent got too steep.

Another factor to watch is the how much the S&P 500 is above the 200 day moving average. I tend to find that if the SPX is ahead of its 200 day simple moving average by much more than 10%, it tends to correct. In 2016 the market fell below its 200 day moving average by more than 15%, and subsequently bottomed. In 2018 the market moved ahead of its 200 day moving average by 15% twice - and subsequently corrected that in both the early and late part of that year. The SPX was around 20% ahead of its moving average before the March 2020 COVID crash. While its easy to blame a market correction on an event, the fact is that an overbought market is always a good setup for that event to hit the market harder than it might have otherwise.

The combination of a parabolic chart that’s currently 15% over that moving average can increase the potential for a correction. The bad news is, that’s where we are now.

There may be one more factor to keep a cautious eye on the markets as we come into the spring. This year, we had a particularly vulnerable race for the Senate in the US electoral process. We noted in prior updates that history suggests market returns are best with a Democrat House (which we just got with the November election) combined with a Republican Senate. Two seats for the Senate went to the Democrats, which was a bit of an upset. Now the balance of power is in favor of the Democrats. That may impact the stock market. Here’s why:

Biden is no friend of big-tech dominance. He noted that anti-trust policies may be considered against some of the leading names in the S&P 500. These include names like Facebook, Amazon, Apple, Google, and Netflix. They all benefitted after the COVID crash in March last year, driving the S&P 500 to new highs. A Democrat Senate will pressure many of these names. The market anticipated that the Republicans could retain the senate, thus tempering the power of the House. However, that anticipation didn’t pan out. This would not just impact the technology sector. It would affect the greater profile of the S&P 500 to some degree. As one institutional manager recently noted on a Bloomberg live chat, a Democrat Senate is: “Negative for stocks; big negative for bonds AND negative for USD… So on a Dem sweep, stocks may rally for a while but then sell off…”

Further, Democrat control will likely mean more stimulus and more spending. Ultimately, this is bullish for stocks so long as that stimulus remains. For this reason, any potential weakness in the nearterm will be a buying opportunity. But it also means that reflation stocks, such as energy, mining, precious metals, and agriculture, will be an even more important part of our longer termed strategy. Those are areas we have been focusing on at ValueTrend.

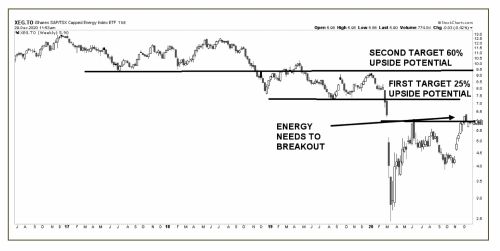

Perhaps the most contrarian of these trades is energy. The market expects a reversal in energy usage in the coming year. “ESG” is all the rage. This is unrealistic. Given production slowdowns and (despite the green movement) continued need for the products, we see an oversold opportunity with significant upside on energy stocks. Much of the demand for fossil fuel is coming from China and India, who are the fastest growing economies in the world. And those countries are paying little attention to the green energy movement. Markets should come back to reality regarding the timeframe needed to eliminate our dependence on oil and gas. Its going to take longer than a year to eliminate our dependence on “black gold”. Meanwhile, the demand for fossil fuels is growing rapidly in the developing nations. Therein lies the opportunity. The chart below for iShares energy producer ETF shows some technical targets if our view is proven correct. In my view, we could have 25% upside on this sector in the next year.

At ValueTrend, we continue to add positions in our Equity Platforms in value names and reflation names as opportunities present themselves. We’ll be keeping a sharp eye on the potential for a market correction after the favorable seasonal period ends in May. By actively managing risk through sector rotation, including the willingness to raise cash when risk appears, we anticipate more upside for our portfolios. Let us hope that 2021 brings us as many opportunities as we had in 2020, without the trauma surrounding the pandemic that created those investment opportunities.

Keith Richards is Chief Portfolio Manager & President of ValueTrend Wealth Mgmt. He can be contacted at info@valuetrend.ca.

Keith Richards may hold positions in the securities mentioned. The information provided is general in nature and does not represent investment advice. It is subject to change without notice and is based on the perspectives and opinions of the writer only. It may also contain projections or other “forward-looking statements”. There is significant risk that forward looking statements will not prove to be accurate and actual results, performance, or achievements could differ materially from any future results, performance, or achievements that may be expressed or implied by such forward-looking statements and you will not unduly rely on such forward-looking statements. Every effort has been made to compile this material from reliable sources; however, no warranty can be made as to its accuracy or completeness. Before acting on any of the above, please consult an appropriate professional regarding your particular circumstances.