A Stand Against Capital Punishment -Ways To Minimize Your Capital Gains Tax Bill Part 1 Basic Principles

When the rubber hits the road and it’s time to sell your investments, all that really matters is what you have left after tipping the tax man, regardless of whether your goal is to fund a once-in-a-lifetime trip, buy your first home or merely pay for groceries. After all the hard work of saving in the first place, managing your investments and minimizing excess fees along the way, failing to do proper tax planning is like forgetting to serve whip cream with pumpkin pie – not a disaster, but still enough of a setback to cause some mild discontented feelings of what could have been. Adding sound tax planning on top of a great investment strategy is the icing on the cake that can make a big difference to your after-tax rate of return. This is one in a three part series designed to do just that. Today’s offering focuses on the basic principles you’ll need to know when doing capital gains planning. As always, all calculations use B.C. tax rates from the current year (2019).

When the rubber hits the road and it’s time to sell your investments, all that really matters is what you have left after tipping the tax man, regardless of whether your goal is to fund a once-in-a-lifetime trip, buy your first home or merely pay for groceries. After all the hard work of saving in the first place, managing your investments and minimizing excess fees along the way, failing to do proper tax planning is like forgetting to serve whip cream with pumpkin pie – not a disaster, but still enough of a setback to cause some mild discontented feelings of what could have been. Adding sound tax planning on top of a great investment strategy is the icing on the cake that can make a big difference to your after-tax rate of return. This is one in a three part series designed to do just that. Today’s offering focuses on the basic principles you’ll need to know when doing capital gains planning. As always, all calculations use B.C. tax rates from the current year (2019).

The Basics

At the risk of stretching my food analogies to the breaking point, some of these ideas may not be a piece of cake to understand but putting in the time now can save you a lot of bread later. To begin, it’s important to understand exactly how capital gains are taxed. The basics are as follows:

- Only 50% of your total gain, net of expenses is added to your taxable income. This usually means paying at least half as much tax per dollar of capital gain compared to interest dollars. This is also true when investing inside a company.

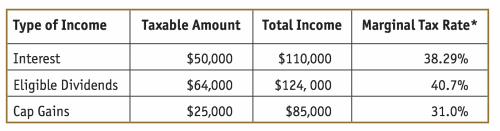

- Since only 50% of your total net gain is added to the mix, this means that you can earn a lot more capital gains in a set tax bracket before getting pushed into higher brackets. For example, assume an investor earns $50,000 in either interest, eligible dividends, or capital gains and $60,000 in net income from all other sources. Only 50% of the capital gains are taxed but eligible dividends are “grossed up” by 138% of their actual payment. Thus, the following chart shows how this hypothetical fifty grand will show up on your tax return for calculating your tax bill and what your total taxable income and marginal tax rate would be when this money is added to $60,000 in other income.

*This column lists the combined Federal and B.C. tax bracket that this taxpayer would inhabit on his last dollar of total income. It DOES NOT show the actual tax rate (s)he would pay on that dollar if it was dividends or capital gains, even though it does provide this information for interest. For capital gains, (s)he would pay 15.5% on that last dollar and for eligible dividends, (s)he would pay 18.88%, ignoring any OAS clawback.

- Capital gains are only taxed when the investment is realized or sold, unlike interest or dividends, which are taxed yearly upon receipt. That means that more of your money is left to compound most of the time when compared to other sources of taxable income, except if receiving dividends in the lower tax brackets, where the payments may be free or even better. Of course, as Moneysaver readers know so well, these dividend payments generally go along with investments that are also realizing capital gains anyway, which is like ordering a pie and getting the ice cream on the side for free.

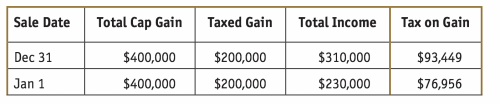

- You can often control when your capital gains bill is triggered, such as when selling rental property or those Tim Horton’s shares you’ve been sitting on for years. That means triggering your gains strategically can reduce how much tax you pay on your capital gain. For example, assume you have the choice of selling your rental property, which has an unrealized capital gain of $400,000 on December 31st in a year where you’re earning $110,000 in other income and one day later, after you’ve retired and expect to earn only $30,000 that year from other sources. Here is what your tax bill on the gains looks like in both scenarios:

But what if this investor owned the property jointly with their spouse who was also making $30,000 and they both sold on Jan 1? In that case, their combined tax bill plummeted to $62,802!

- You can apply 50% of any capital losses you’ve realized in the past but not yet written off against gains you realize that year. If realizing any losses this year, after offsetting them against that year’s gains, you can carry them back against gains you’ve earned in the 3 prior years or carry them forward indefinitely to use against future gains or against other income if any are still on the books at your death.

- When selling only some of a fund or individual stock in a non-registered account, while hanging onto some until later, the tax bill gets calculated by averaging all of your purchases of that asset so that you are taxed proportionately, rather than looking at each sale or purchase individually. Thus, if you sell 40% of your shares in a restaurant fund in your non-registered account, you would include 40% of the total gain of all the shares you own, regardless of when you purchased them.

- Capital gains inside your RRSP and RRIF are like all your other RRSP and RRIF investments – taxed as income only upon withdrawal or death. Capital gains inside your TFSA are tax-free in all instances, just like any other type of income earned inside that account. That means there are no special rules for capital gains in these instances. If transferring shares you own in your non-registered account to a registered account, you trigger capital gains at that time as if you’d sold the shares instead. It is often a bad idea to transfer shares with losses to these accounts in kind, as you won’t get credit for the capital loss. Instead, consider selling the assets and either waiting 31 days to repurchase them in your registered account (or your spouse’s name or so on) or buy a similar but not identical investment inside your registered accounts if the capital loss is large enough. I talk more about this more in my later articles when discussing the “superficial loss rules.”

Conclusion

Today’s article is merely the appetizer for the far more sumptuous main course where you can put some of these principles into action.

Colin S. Ritchie, BA.H. LL.B., CFP, CLU, TEP and FMA is a Vancouver-based fee-for-service lawyer and financial planner who does not sell investment or insurance, just advice. To find out more, visit his website at www.colinsritchie.com.