Critical Illness Insurance Explained

I was speaking today with an investment advisor about the value of critical illness insurance. He said, “I don’t need that coverage as the likelihood of me having a critical illness is very low.” Really? In the financial services profession only 22% of people are active in providing their clients with critical illness insurance advice.

I was speaking today with an investment advisor about the value of critical illness insurance. He said, “I don’t need that coverage as the likelihood of me having a critical illness is very low.” Really? In the financial services profession only 22% of people are active in providing their clients with critical illness insurance advice.

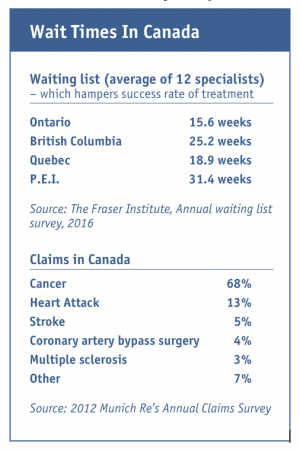

I ask you this: Do you know anyone who has suffered any of these conditions: cancer, heart attack, stroke, ALS, Parkinson’s or has had a loss of independence?

Critical illness contracts can be complex for advisors who do not have knowledge of contractual obligations; in my opinion, this is one of the reasons why this product is rarely presented. These contracts are specific in their definitions of what is covered, and it may seem to some people that insurance companies are trying not to pay claims. This is an inaccurate assessment.

Some say the product can be expensive and they are correct. The cost is based on premium structure and contract type. The probability of a critical illness occurring before age 75 is five times more likely to occur than a person dying before age 75; this is reflected in the premium insurance companies charge. There are various types of critical illness policies on the market with variable terms such as Term 10 (in effect for 10 years), 20 (in effect for 20 years), 75 and Term to 100. The Term 10 and Term 20 contracts are renewable and convertible to a permanent plan and initially are more affordable. However, they renew at a higher rate without the need for another medical assessment, making them less affordable down the road.

There are a number of riders you can attach to a critical illness policy, such as a Return of Premium on Death. This rider will refund 100% of the premium paid into the policy to your beneficiary if you die and if no critical illness claim has been paid out. Inexperienced advisors sell a Return of Premium after 15 years. If you have not had a claim after 15 years or you have to cancel the policy to get the refund. In this option your premium can be double the base premium, and when a claim is paid on a critical illness, the extra premium is left as a gift to the insurance company. This, in my opinion is a terrible option.

Education in the insurance industry is improving, however there are very large variances, so ask your advisor for their credentials. We not only represent leading insurance companies, we also help clients receive successful claim payments. You may want to ask the individual you are working with how may claims they settled and what do they do for their clients at claims t ime.

ime.

Unfortunately, critical illness coverage is probably the most difficult policy to get because family history as well as your personal health play significant roles. Never assume that you will not qualify and that all companies underwrite and accept a risk the same way; work with an advisor as who represents at least three insurance companies.

Critical illness insurance can be the best investment you make, because when you are stricken with a qualified condition and survive, a cheque is on its way. Do not confuse disability insurance and critical illness claim payment. Critical Illness claim occurs with a diagnosis of one of the covered conditions and you must survive for a period of 30 days before a cheque is issued. Often people confuse disability insurance requirements of not being able to work to that of a critical illness contract which pays you even if you can work. Critical Illness insurance is more complex then any other life product in my opinion therefore it is important to gain full understanding of what is covered and how is a claim defined like “cancer”. Work with a knowledgeable adviser who represents multiple insurance companies and ask for explanations of contractual definitions.

Reality Check

Cancer

Source: The Canadian Cancer Society1

- An estimated 206,200 new cases of cancer and 80,800 cancer related deaths occurred in Canada in 2017

- Approximately 103,200 Canadian women and 103,100 Canadian men will be diagnosed with cancer and an estimated 38,200 women and 42,600 men will die of cancer.

- 1 in 2 Canadians will develop cancer in their lifetime

- 1 in 8 women will develop breast cancer

- 1 in 2.2 women and 1 in 2 men will develop cancer in their lifetime

Heart Attack

Source: The Heart and Stroke Foundation

- 1 in 4 Canadians will contract some form of heart disease

- 75,000 Canadians suffer a heart attack each year

- For every 100 people who have a stroke:

- 5 die (15%)

- 10 recover completely (10%)

- 25 recover with a minor impairment or disability (25%)

- 40 are left with a moderate to severe impairment (40%)

- 10 are so severely disabled they require long-term care (10%)

- Heart disease costs the Canadian economy approximately $19 billion every year in medical services, hospitalization expenses, loss of income and loss of productivity

- The rate of death among patients hospitalized from heart attacks has been decreased by half, from 16% to 8%

- 1 in 2 heart attack victims is under age 65

Stroke

Source: The Heart and Stroke Foundation

- 50,000 Canadians suffer a stroke each year

- 75% survive the initial event

- Strokes are the leading cause of neurological disability

- 1/3 of stroke victims are under the age of 65

- 60% of stroke victims will be left with a disability

Multiple Sclerosis

Source: The Multiple Sclerosis Society of Canada

- More than 50,000 Canadians have MS

- MS is the most common neurological disease among young Canadians

- Canadians have one of the highest rates of MS in the world

- Women are twice as likely to develop MS as men

Parkinson's Disease

Source: The Parkinson's Foundation of Canada

- 30% of all Parkinson's patients are under 50

- 20% of all Parkinson's patients are under 40

- There are approximately 80,000-100,000 Canadians suffering from Parkinson's

Paralysis

Source: The National Spinal Cord Injury Association of Canada

- There are an estimated 900 Canadians who sustain a spinal cord injury each year

- More than 30,000 Canadians suffer from paralysis of 2 or more limbs

- Most persons who suffer spinal cord injury are between 16 and 20 years of age

- The most common causes of spinal cord injury are car collisions and falls

Alzheimerís Disease2

Source: The Canadian Alzheimer’s Society

- In 2016, Alzheimer’s disease was the seventh leading cause of death in Canada

- There are currently 564,000 Canadians living with Alzheimer’s Disease. That number is expected to rise to 937,000 by 2033

- There are approximately 25,000 new cases of Alzheimer’s Disease diagnosed each year

- 65% of people diagnosed with Alzheimer’s Disease are women over the age of 65

- 16,000 people diagnosed with Alzheimer’s Disease are under the age of 65

Kidney Failure

Source: The Kidney Foundation of Canada

- Kidney disease ranks sixth among diseases causing death in Canada

- Each day an average of eight Canadians learn that their kidneys have failed

- At the end of 2016, approximately 3421 Canadians were on a waiting list for kidney transplant. (Source: Annual Statistics on Organ Replacement in Canada, 2007 to 2016 https://www.cihi.ca/sites/default/files/document/corr_ar-snapshot-en.pdf)

- 1731 kidney transplants were performed in Canada in 2016

- 1 in 10 will develop kidney stones at some point in their lives

Milan Topolovec, BA, TEP, CLU, CHS, RCIS

President & CEO, TK Financial Group Inc.

1 Canadian Cancer Society. Canadian Cancer Statistics, A 2018 special report on cancer incidence by stage, June 2018. http://www.cancer.ca/~/media/cancer.ca/CW/cancer%20information/cancer%20101/Canadian%20cancer%20statistics/Canadian-Cancer-Statistics-2018-EN.pdf?la=en

2 Larry W. Chambers, Christina Bancej and Ian McDowell. Prevalence and Monetary Costs of Dementia in Canada. (Toronto: The Alzheimer Society of Canada in collaboration with the Public Health Agency of Canada Toronto, Ontario, Canada 2016) http://alzheimer.ca/sites/default/files/files/national/statistics/prevalenceandcostsofdementia_en.pdf