Looking For The True Market Top

In light of the Q1 pullback that occurred this year, we have received a number of calls from clients concerned about the possible crest in the secular bull market. After all, the upward trend in the markets has lasted nine years. Many of the “talking heads” and market “gurus” on the financial networks and online have said: “This is likely the top. How much longer can it last?”.

In light of the Q1 pullback that occurred this year, we have received a number of calls from clients concerned about the possible crest in the secular bull market. After all, the upward trend in the markets has lasted nine years. Many of the “talking heads” and market “gurus” on the financial networks and online have said: “This is likely the top. How much longer can it last?”.

One of the key functions of writing these articles is to provide investors with the tools to make their informed decisions.

Market tops, like market bottoms, are often challenging to try and pinpoint (market commentators will always try), but the true peak will always leave certain clues behind. And that is what this article is all about.

First, fundamentals (Price/Earnings or P/E ratio), in our opinion, does not offer enough of a timing tool. It is usually six to nine months behind the market crest. For example, in the last major market peak in the 1st quarter of 2008, fundamentals didn’t start to flash danger until mid-2008. By that time, much of the market damage had already played out.

Technicals can be challenging for individuals to interpret. And with so many indicators, which ones have more validity? Even the experts read the data differently.

Economics is our last category and this group can be the most confusing. Many economic indicators will contradict each other and send the investor into a tailspin. Nevertheless, we feel there are some key indicators that are easy to understand and provide, what we believe, is another important part of the analysis picture.

The U.S. unemployment rate and the U.S. yield curve have the best timing connection to the stock market. The unemployment rate moves in the opposite direction to the markets and usually lags the market by a few months. At this point (early May), the index is still heading down. The unemployment rate just reached a 9-year low of 3.9 percent. https://tradingeconomics.com/united-states/unemployment-rate.

![]()

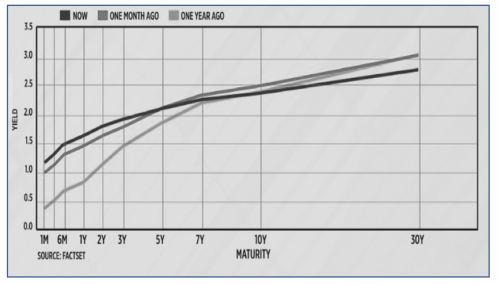

The U.S. yield curve is one of the most reliable indicators we have found for equity indexes and leads the markets by about six to nine months. The function of this gauge for investors is to illustrate when the markets have room to advance, when they are near the top and when the markets are expected to start a bear decline. The angle of the curve is the clue. A normal yield curve is one where short-term rates are lower than long term rates. This indicates that the Fed has ample room to adjust the short-term rates to keep the economy moving forward. This normal position is good for the markets and investors. A flat curve is when the Fed has continued to raise the short-term rates to “cool” the rapidly expanding economy and try to keep it from overheating. This is a time where markets are near the crest and investors should start adjusting their portfolios to be more conservative (using stop loss positions, fixed income, and building up cash). The next move for the yield curve is when short-term rates are higher than long term bond returns. This occurred in 2000 and 2007. When an inverted rate curve happens, the markets are on “life support” and investors may wish to become defensive.

Bottom line:

At this junction, the curve is in a normal position indicating the Fed has room to adjust the rates as the U.S. economy dictates. It also suggests that there is more upside potential for the markets. Economics is an area that most investors don’t employ in their market analysis, but it can provide key information that fundamentals and technicals does not offer. A great free source for economic data is on the website: www.tradingeconomics.com.

Donald W. Dony, FCSI, MFTA. Analyst, past instructor for the Canadian securities institute (CSI), editor for the www.technicalspeculator.com, dwdony@shaw.ca, 250-479-9463