The Old Dow Versus The New Dow

Investors should be nervous about today’s “modern” Dow Jones Industrial Average because this is not the same Dow your daddy used to own.

Investors should be nervous about today’s “modern” Dow Jones Industrial Average because this is not the same Dow your daddy used to own.

The problem with today’s Dow Jones Industrial Average is that unlike the 1980s Dow, today’s Dow is no longer “industrial”. The “old” Dow of the 1980s had 18 industrial-related components, while the new or “modern” Dow of today has only six industrial-related components. The new Dow has gone “consumer” with 12 consumer-related components – double that of the old Dow.

The Dow transition from old to new has serious implications for investors because the old Dow was economy-sensitive and the new Dow is interest-rate-sensitive.

This is a need-to-know because of the relevance of the Dow is an important bellwether.

The Dow Jones Industrial Average (DJII) is one of the oldest continual stock groups in the modern investing world. (Actually the Dow Jones Transportation Average is the oldest—1884). The DJII was founded by Charles Dow in 1896 and represented the dollar average of 12 stocks from leading American industries.

The original group of 12 stocks ultimately chosen to form the Dow Jones Industrial Average did not contain any railroad stocks, only purely industrial stocks. Of these, only General Electric currently remains part of that index.

The Dow Was Originally A Made-In-America Basket Of Industrial Companies.

Today the Dow is among the most closely watched U.S. benchmark indices tracking targeted stock market activity. Although Charles Dow initially compiled the index to gauge the performance of the industrial sector within the American economy, the evolution of the modern multinational corporation has now made the Dow a global bellwether.

According to S&P DOW JONES INDICES (S&P), the Dow is a historical investment bellwether and the Dow Jones Industrial Average is one of the best-known icons of American culture among stock market observers around the world.

S&P also explains, “While stock selection is not governed by quantitative rules, a stock typically is added to The Dow only if the company has an excellent reputation, demonstrates sustained growth and is of interest to a large number of investors. Maintaining adequate sector representation within the indices is also a consideration in the selection process.”

The Dow transformation from old to new began slowly through the late 1980s and early 1990s and was virtually completed when, on November 1, 1999, Microsoft Corp, Intel Corporation, SBC Communications and Home Depot Incorporated replaced Chevron Corp, Goodyear Tire & Rubber, Union Carbide and Sears, Roebuck.

To better understand the significance between today’s new or modern Dow and the old Dow, we need to go back thirty years ago when the “buy of a generation” was signalled in the Dow Jones Industrial Average.

I selected December 1984 to be the “buy of a generation” because technically at 1200 the Dow was firmly above 15 years of price congestion at the 1000 price level. The fundamentals were also positive as we were approaching the mid-point of the Reagan Administration (January 20, 1981 to January 20, 1989), a government that was an advocate of free markets and laissez-faire economics.

A 30-year buy-and-hold strategy on the Dow from December 1984 through to December 2014 would, excluding dividends, have a capital return of 1400 percent for an annualized return of about 9.4 percent. Quite remarkable when you include some major bear markets such as the Black Monday Liquidity Crisis of 1987, the 1990 Iraq invasion of Kuwait Crisis, the Asian Financial Crisis of 1997, the dot-com bubble and Y2K panic of 2000 and the 2007-2008 global financial crisis.

The OLD Dow:

A 15-year buy-and-hold strategy on the “old” Dow from December 1984 through to December 1999 would, excluding dividends, have a capital return of 858 percent for an annualized return of about 16 percent. That was the period when buy-American referred to U.S.-made goods such as autos and auto parts, clothing, machinery, appliances, tools and other stuff like office supplies and furniture.

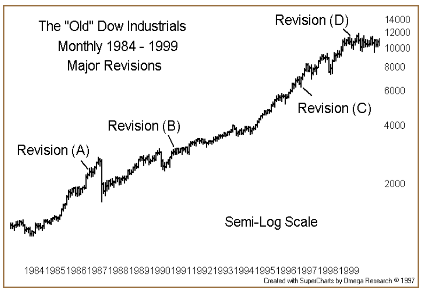

Our 15-year chart of the old, economy-sensitive Dow from 1984 through to 1999 displays the gradual removal of the industrial components and the shift to the modern, interest-sensitive Dow that began in 1987 (shown as A below) with the revision of March 12, 1987 that had Coca-Cola and Boeing Company replace Owens-Illinois Glass and Inco.

The revision of May 6, 1991 at (B) had Caterpillar Inc, Walt Disney Co and J.P. Morgan & Co replace Navistar International Corp., USX Corporation and Primerica Corporation

The revision of March 17, 1997 (shown at C) had Travelers Group, Hewlett-Packard Company, Johnson & Johnson and Wal-Mart Stores replace Westinghouse Electric, Texaco Incorporated, Bethlehem Steel and Woolworth.

The big revision to de-industrialize the Dow occurred on November 1, 1999, just months before the technology crash—shown at D—when Microsoft Corp, Intel Corporation, SBC Communications and Home Depot Incorporated replaced Chevron Corp, Goodyear Tire & Rubber, Union Carbide and Sears, Roebuck.

The NEW Dow:

A 15-year buy-and-hold strategy on the “new” Dow from December 1999 through to December 2014 would, excluding dividends, have a capital return of 55 percent for an annualized return of about 3 percent.

Our 15-year chart of the new Dow from 1999 through to 2014 displays the persistent shift away from industrial-related components to consumer-related components when on April 8, 2004 (shown at A below) AT&T, Eastman Kodak, and International Paper were replaced by American International, Pfizer, and Verizon. This transition from industrial to consumer continued when on June 8, 2009 (shown at B), Citigroup and General Motors were replaced by Cisco Systems and Travelers.

The final transition from the original 1984, 18 industrial names to the current six industrial names occurred on September 2013 (shown at C) when Goldman Sachs, Visa and Nike were added to the Dow Jones Industrial Average, to replace Hewlett-Packard, Bank of America and Alcoa.

The last Dow transition from the “old” industrial-sensitive to the “modern” consumer-sensitive Dow occurred March 6, 2015 when Apple Inc. joined the Dow Jones Industrial Average replacing AT&T Inc.

Strategy:

The great 2009 – 2014 advance in the Dow to new all-time highs was led by the consumer-related companies such as The Walt Disney Company, The Home Depot, Inc., The Coca-Cola Company, McDonald's Corp., Nike Inc., Visa Inc. and Wal-Mart Stores Inc.

This makes the current Dow behave like the SPDR Consumer Discretionary sector (XLY) which is basically a basket of companies that sell goods to Americans made somewhere else. The XLY has been a direct beneficiary of low interest rates and, more recently, lower crude and gasoline prices. This in turn has global investors bidding up U.S. equities and chasing the U.S. dollar

If you believe—as I do—that the current global expansion will continue, then any gradual rise in crude prices and interest rates will only confirm the reality of global expansion.

In other words, while a gradual rise in crude prices and interest rates may not be good for the “new” consumer-sensitive Dow, exporting nations such as Germany, South Korea and Japan may be direct beneficiaries.

This may be an early call but Canadian investors who are overweight in U.S. equities may be prudent to reduce U.S. exposure and boost their global exposure by taking advantage of the many TSX listed “global” exchange traded funds (ETFs).

Below are some ETFs to get you started – both iShares and BMO have websites or, for more information speak to an advisor who has a securities license.

Bill Carrigan, CIM is an independent stock-market analyst. He can be reached at: info@gettingtechnical.com